담보 평가 사각지대: 자이랜드가 어떻게 다르게 접근하는가

< English follows Korean >

2025년 8월부터 2026년 3월 사이 국내 주요 보증기관의 감정평가 신청자 10명 중 6.5명이 본감정 단계 전에 취소했습니다. 감정평가액이 실거래 시세보다 20~30% 낮게 산정되어 보증 가입이 불가능해졌기 때문입니다. 그 여파는 청년임대주택 보증 갱신 거절과 일부 임대사업자 법정관리로 이어졌습니다.

반대 방향의 실패도 있었습니다. 2023년 이전 시세를 부풀리는 ‘업감정’이 전세사기의 발판이 됐습니다. “원하는 금액을 맞춰드릴 수 있다”는 광고가 관련 앱에 이틀에 한 번꼴로 올라왔습니다.

과소 평가와 과대 평가. 두 실패의 원인은 같습니다 – 독립적인 가격 참조 기준이 없다는 것. 이 글은 그 구조적 공백을 어떻게 채울 수 있는지 그리고 자이랜드가 지금 실제로 무엇을 제공하는지에 대한 이야기입니다.

📌 기관 유형별

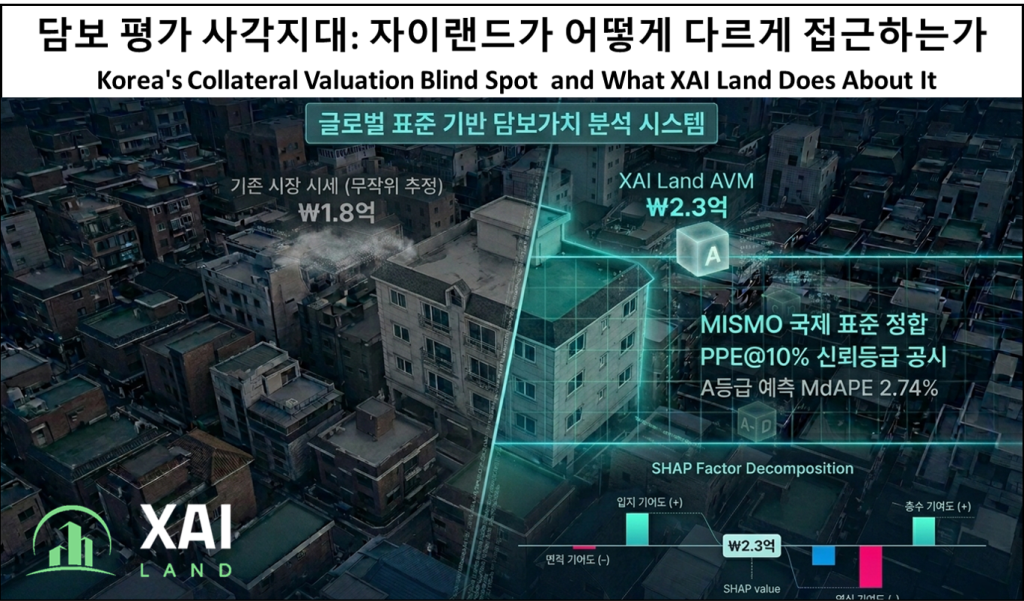

같은 물건, 다른 가격 – 울산의 경우

추상적인 이야기를 구체적으로 만들어 보겠습니다. 2025년 울산에서 실제로 거래된 한 빌라 물건을 보면 HUG 인정감정평가 결과는 약 1.8억 원으로 산정됐습니다. 그런데 자이랜드 AVM은 동일 물건을 2.3억 원으로 추정했고 실제 인근 거래 사례도 2억 원 이상에서 형성되어 있었습니다. 결과는 보증 탈락이었습니다. 실제 시장에 거래가 존재하는 물건이었는데도요.

울산의 HUG 예비감정 취소율은 90%였습니다. 경북 74.3%, 충북 74.3%로 이어집니다. 이 지역들에서 가격이 실제로 없어서 보증이 안 된 게 아니라 – 가격을 측정하는 기준이 없어서 안 된 겁니다.

독립적 AVM 참조 레이어가 있었다면 이 편차는 심사 전에 탐지됩니다.

±10% 이내. MISMO 기준이 의미하는 것

미국 모기지산업표준기구(MISMO)가 2025년 7월 제정한 국제 기준은 PPE@10% – 추정가가 실거래가의 ±10% 이내에 포함된 비율을 핵심 지표로 씁니다. 개별 물건 단위의 신뢰도를 묻는 지표입니다. 자이랜드는 이 기준을 충족합니다.

출처: 자이랜드 avm_pipeline v2.0 표본외 테스트 (2026.03) · 193,325건 실거래 검증 · 틸 = MISMO 80% 충족 / 회색 = 미충족

아파트 81.6%, 단독/다가구 86.9% – 두 모델 모두 MISMO 기준을 상회합니다. 전국 193,325건의 실거래를 학습에 사용하지 않은 표본외 데이터로 검증한 수치입니다. 국내에서 이 수준의 정확도를 공개하는 AVM 서비스는 자이랜드뿐입니다.

비교 기준이 있습니다. 2024년 도쿄 콘도미니엄 5개 AVM 서비스 비교 연구(Ota & Uto)에 따르면, 동일 자산에 대한 서비스 간 평균 가격 편차가 10.6%에 달했고 어떤 서비스도 정확도를 공시하지 않았습니다. 한국도 현재 같은 상황입니다.

신뢰등급 A–D: 모르는 것을 아는 것

평균 정확도보다 더 중요한 질문이 있습니다.

어떤 물건에서 모델이 틀릴 가능성이 높은가?

아파트 기준으로 Grade A 예측의 MdAPE는 2.74%, Grade D는 6.33%입니다. 같은 숫자로 다루는 건 위험합니다.

출처: 자이랜드 avm_pipeline v2.0 (2026.03) · 128,862건 아파트 표본외 테스트 · 등급 간 단조 감소(monotonically decreasing) 패턴은 신뢰등급 시스템이 정상 작동함을 의미합니다

이 등급 시스템이 하는 일은 하나입니다. 모델이 언제 자신을 신뢰해야 하는지 스스로 판별합니다. 금융감독원이 묻는 “이 시스템이 언제 실패하는지 알고 있는가?”라는 질문에 대한 제도적 답변입니다. 2026년 1월 시행된 AI기본법의 고영향 AI 설명가능성 요건에도 직접 대응합니다.

세 가지 제품, 하나의 리스크 아키텍처

자이랜드의 세 제품은 독립적으로도 순차적으로도 사용할 수 있습니다.

LENS (가치보고서) – 개별 물건 검증. 특정 담보물에 대해 AVM 추정가, 신뢰등급(A–D), SHAP 기반 요인 분해(입지·면적·연식·층수)를 제공합니다. “이 물건 가격이 왜 이 수준인가”에 답할 수 있게 됩니다. 보증 심사 전 교차 검증, 대출 심사 시 설명 근거로 즉시 활용 가능합니다. IT 연동 없이 파일럿 시작 가능.

VAULT (담보 리스크 플랫폼) – 포트폴리오 전체 모니터링. 기관이 보유한 담보 포트폴리오 전체를 자산 유형·지역·신뢰등급 분포로 실시간 추적합니다. 부실이 NPL로 드러나기 전에, 어느 지역의 Grade D 비중이 높아지는지를 확인합니다. FSS 검사 대응용 감사 로그 자동 생성.

RADAR (조기경보 시스템) – 시스템 리스크 감시. 대한민국 주택 시장 전체의 이상 신호를 위기가 되기 전에 감지합니다. 주택금융·보증·정책·감독 기관을 위한 거시적 리스크 인텔리전스 대시보드입니다. 특정 금융기관의 지분이나 이해관계가 없는 중립적 위치에서 공공 지표를 교차 검증합니다.

개별 검증(LENS) → 포트폴리오 통제(VAULT) → 조기경보 시스템(RADAR). 같은 AVM 엔진, 같은 신뢰등급 체계. 어디서 시작하든 연결됩니다.

자이랜드는 특정 금융기관, 시세 플랫폼, 또는 개발사와의 자본의존 관계 없이 독립적으로 운영됩니다. 이러한 구조적 독립성이 있기 때문에, 자이랜드는 AVM 정확도를 외부 기준에 맞춰 투명하게 공시할 수 있습니다.

왜 지금인가 – 제도적 배경

한국의 주요 주택금융 공공기관 중 하나가 2025년 12월, 2026~2028년 AI 전환(AX) 전략을 발표하며 AVM을 리스크 관리 및 전세사기 예방에 활용하겠다고 명시했습니다. 2026년 내 시범 운영, 2027년 이후 확대가 공개 계획에 담겨 있습니다.

AI기본법은 2026년 1월 22일 시행됐습니다. 대출 심사에 활용되는 AI 시스템은 “고영향 AI”로 분류되어 설명가능성이 요건입니다. MISMO CCS 기준은 2025년 7월 제정됐습니다. 제도적 지형이 빠르게 바뀌고 있습니다.

AVM을 도입하기로 결정했다면, 다음 질문은 하나입니다 – 그 AVM이 얼마나 정확한지, 어디서 불확실성이 높아지는지 알 수 있는가? 이것이 공개 정확도 공시의 의미입니다.

왜 ‘독립성’이 정확도만큼 중요한가

AVM의 정확도만큼 중요한 요소가 하나 더 있습니다. 바로 평가 구조의 독립성입니다.

현재 국내 시장에서는 △금융기관 △시세·데이터 플랫폼 △개발사 및 중개 플랫폼이 다양한 방식으로 연결되어 있는 경우가 많습니다. 이 과정에서 AVM 제공자가 특정 이해관계자와 자본, 수익, 또는 사업적으로 연결되어 있을 경우 평가 결과가 완전히 독립적인 시장 기준을 반영하는지에 대한 질문이 자연스럽게 발생합니다.

이러한 구조는 평상시에는 큰 문제로 드러나지 않을 수 있습니다. 그러나 시장 변동성이 확대되는 시점에서는 작은 편향도 누적되어 담보 과대평가 또는 과소평가로 이어질 수 있으며 이는 곧 금융 리스크로 연결됩니다.

해외에서도 유사한 문제가 관찰됩니다. 일본 도쿄 지역을 대상으로 한 연구에서는, 서로 다른 5개의 AVM 서비스 간 동일 자산에 대해 평균 10% 이상의 가격 차이가 발생했으며, 대부분의 서비스는 정확도 공시를 제공하지 않았습니다. 이는 “어떤 AVM을 기준으로 삼아야 하는가”라는 질문이 기술 문제가 아니라 신뢰 구조의 문제임을 보여줍니다.

결국 핵심은 하나입니다. AVM이 얼마나 정확한가뿐만 아니라 그 정확도를 신뢰할 수 있는 구조 위에서 제공하고 있는가입니다. 그래서 글로벌 기준에서는 “정확한 모델”보다 “이해상충이 없는 구조”를 먼저 요구합니다.

빌라는 왜 다른 방식으로 공시하는가

연립·다세대 파이프라인 통계를 공개하지 않습니다. 예측구간 폭이 아파트의 약 3배인 시장에서 파이프라인 수치를 그대로 내놓는 건 정밀도의 환상을 줄 위험이 있습니다. 대신 2025년 5월 연립·다세대 실거래 6,000건을 기준으로 주요 시세 시스템과 직접 비교한 독립 백테스트 결과를 공시합니다. 자이랜드 전국 MdAPE 5.4%, 서울 2.9%. 이 결과는 2025년 9월 국회 정책포럼에서 발표됐고, 독립 동료심사 논문에도 수록돼 있습니다.

좋아 보이는 숫자와 방어 가능한 숫자는 다릅니다. 저는 두 번째를 선택했습니다.

참고자료

[1] 연합뉴스, “평가액 너무 낮아…HUG 인정감정평가 신청자 65%가 중도 취소,” 2025.10.12

[2] 머니투데이, “전세사기 뺨 맞은 국토부·HUG…청년주택에 감정가 ‘20% 룰’ 씌웠다,” 2025.09.15

[3] 데일리안, “[단독] 감정평가액 과도하게 낮아 불만에…HUG 제도 개선 나선다,” 2026.03.16

[4] KBS 뉴스, “원하는 대로 맞춰드려요…전세사기 징계에도 여전한 ‘업감정’,” 2023.03.23

[5] 연합인포맥스, “경실련 ‘LH 매입 가격 개선 방안…고가 매입 해결 못해’,” 2026.03.19

[6] 구강모·임동준, 「자동가치산정의 정확성 분석 및 투명성 관리 방안」, JREA Vol.10 No.3, 2024. DOI 10.30902/jrea.2024.10.3.177

[7] MISMO, Common Confidence Score (CCS) Standard, July 2025

[8] 파이낸스뉴스, “[기획] 부동산 가치평가 개혁 골든타임…금융·AVM·정부 간 이해상충 위험,” 2025.12.15

자이랜드는 한국 주거용 부동산 시장에서 ‘독립적인 가격 참조 레이어’를 구축하는 AVM 인프라 기업입니다. 감정평가 의존 구조에서 발생하는 과대·과소 평가 문제를 해결하고, 금융기관이 담보가치를 일관되고 검증 가능하게 판단할 수 있도록 합니다.

금융기관·정부기관 대상 담보 리스크 관리, 포트폴리오 모니터링, 시장 인텔리전스 솔루션을 제공합니다. SHAP 기반 설명가능성 · A–D 신뢰등급 · MISMO CCS 정합 아키텍처를 기반으로, FSS 검사 및 AI기본법 요건에 대응 가능한 시스템을 구축합니다.

정확도 공시: xai.land/accuracy · 문의: contact@xai.land · 웹사이트: xai.land

Korea’s Collateral Valuation Blind Spot and What XAI Land Does About It

Between August 2025 and March 2026, 65% of applicants to Korea’s major housing guarantee institution abandoned their appraisal mid-process. Appraisals were coming in 20–30% below market prices. The fallout: youth rental housing lost insurance coverage, some operators filed for court receivership.

The opposite failure ran for years before that appraisers being engaged to inflate valuations, which became the structural foundation of jeonse fraud affecting tens of thousands of tenants.

Both failures trace to the same gap: no independent, verifiable price reference layer. This post explains what XAI Land builds and how institutions can use it now.

📌 By institution type

Same Property, Different Price – The Ulsan Case

Concretely: a villa property in Ulsan in 2025 received an HUG certified appraisal valuation of approximately ₩180 million. XAI Land’s AVM estimated the same property at ₩230 million consistent with nearby comparable transactions. The result was guarantee rejection, for a property with active market activity around it.

Ulsan’s HUG appraisal abandonment rate was 90%. North Gyeongsang: 74.3%. North Chungcheong: 74.3%. In these markets, the problem wasn’t that prices don’t exist…it’s that the reference system couldn’t find them. An independent AVM layer detects this divergence before the application fails.

The MISMO Threshold and Where XAI Land Stands

The Mortgage Industry Standards Maintenance Organization (MISMO)’s July 2025 standard defines PPE@10% – the proportion of predictions landing within ±10% of actual transaction price as the core benchmark for mortgage-grade AVMs. XAI Land’s apartment model: 81.6%. Dandok: 86.9%. Both clear the 80% threshold. Based on 193,325 out-of-sample real transactions.

No other Korean AVM provider publishes this. Accurate reference pricing requires a verifiable source – not a marketing claim.

For context: a 2024 study comparing five AVM services for Tokyo condominiums (Ota & Uto) found an average price divergence of 10.6% across services for the same property and none of them disclosed their accuracy. Korea is currently in the same position.

Source: XAI Land avm_pipeline v2.0 out-of-sample test (March 2026) · 193,325 real transaction validations · Teal = meets MISMO 80% threshold / Gray = below threshold

Apartments: 81.6%, Single-family/Multi-family homes: 86.9% – Both models exceed the MISMO standard. These figures were validated using out-of-sample data comprising 193,325 actual transactions nationwide that were not used in the training process. XAI Land is the only AVM service in Korea to publicly disclose this level of accuracy.

Confidence Grades: The System That Knows What It Doesn’t Know

For apartments, Grade A predictions carry a MdAPE of 2.74%. Grade D: 6.33%. Treating both identically in a credit decision creates systematic risk in one direction – over-lending on weak collateral or systematic inefficiency in the other: excessive conservatism on solid collateral.

Source: XAI Land avm_pipeline v2.0 (March 2026) · 128,862 apartment out-of-sample tests · The monotonically decreasing pattern across grades indicates a properly functioning confidence grading system

The confidence grade answers the FSS examiner’s core question: does your system know where it fails? Under Korea’s AI Basic Act (effective January 2026), high-impact AI systems used in loan decisions require this level of explainability. The grade is the audit trail.

Three Products, One Risk Architecture

XAI Land’s three products can be used either independently or in sequence.

LENS (Valuation Report) delivers, for a single property: AVM estimate, Confidence Grade, and SHAP factor breakdown (location, size, age, floor). The loan officer can explain the valuation. No system integration required to pilot.

VAULT (Collateral Risk Platform) monitors an institution’s entire collateral portfolio in real time — by property type, region, and confidence grade distribution. Surface NPL risk before it crystallizes in the data.

RADAR (Early Warning System) detects anomalies across the entire South Korean housing market before they turn into a crisis. It is a macro-level risk intelligence dashboard for housing finance, guarantee, policy, and supervisory institutions. From a neutral standpoint, completely free of any equity or vested interests in specific financial institutions, it cross-verifies public indices.

Individual Verification (LENS) → Portfolio Control (VAULT) → Early Warning System (RADAR). Same AVM engine, same confidence grading system. Wherever you start, it’s all connected.

XAI Land operates independently, without equity dependency on financial institutions, pricing platforms, or developers. This structural independence is what allows us to publicly disclose AVM accuracy against external benchmarks.

The Institutional Moment

One of Korea’s major public housing finance institutions published a 2026–2028 AI Transformation roadmap in December 2025 explicitly naming AVM for risk management and jeonse fraud prevention. The direction is set. The question is which AVM, and whether it can prove its accuracy before deployment.

Korea’s AI Basic Act is in force. MISMO’s CCS standard is published. The regulatory and technical frameworks are converging. Institutions that build AVM capability now will be ahead of the FSS audit curve, not scrambling to catch up.

Why Independence Matters as Much as Accuracy

There is a second question, as important as accuracy: structural independence.

In many markets, AVM providers are connected through equity, or strategic partnerships to financial institutions, pricing platforms, or developers. When valuation providers operate within these ecosystems, a natural question arises: is the output fully independent of the interests tied to it?

These structural links may not create visible issues in stable markets. But during periods of stress, even small biases can compound into systematic overvaluation or undervaluation directly translating into financial risk.

International evidence points to the same concern. A study of five AVM services in Tokyo found average price divergence exceeding 10% for the same assets, with no public accuracy disclosure from most providers. This highlights that the issue is not just model performance, but whether the system producing the valuation can be trusted.

The question, ultimately, is not only how accurate an AVM is, but whether that accuracy is produced within a structure that can be independently verified. This is why global standards prioritize conflict-free structure before model performance.

Why are villas disclosed differently?

We do not disclose pipeline statistics for townhouses and multi-family homes. In a market where the prediction interval is approximately three times wider than that for apartments, simply releasing pipeline figures risks creating a false impression of precision. Instead, we publish the results of an independent backtest that directly compares our model with major market price systems, based on 6,000 actual transactions for townhouses and multi-family homes in May 2025. Ziland’s nationwide MdAPE is 5.4%, and 2.9% for Seoul. These results were presented at the National Assembly Policy Forum in September 2025 and have been published in a peer-reviewed journal.

A number that looks good is different from a number that’s defensible. I chose the latter.

참고자료

[1] 연합뉴스, “평가액 너무 낮아…HUG 인정감정평가 신청자 65%가 중도 취소,” 2025.10.12

[2] 머니투데이, “전세사기 뺨 맞은 국토부·HUG…청년주택에 감정가 ‘20% 룰’ 씌웠다,” 2025.09.15

[3] 데일리안, “[단독] 감정평가액 과도하게 낮아 불만에…HUG 제도 개선 나선다,” 2026.03.16

[4] KBS 뉴스, “원하는 대로 맞춰드려요…전세사기 징계에도 여전한 ‘업감정’,” 2023.03.23

[5] 연합인포맥스, “경실련 ‘LH 매입 가격 개선 방안…고가 매입 해결 못해’,” 2026.03.19

[6] 구강모·임동준, 「자동가치산정의 정확성 분석 및 투명성 관리 방안」, JREA Vol.10 No.3, 2024. DOI 10.30902/jrea.2024.10.3.177

[7] MISMO, Common Confidence Score (CCS) Standard, July 2025

[8] 파이낸스뉴스, “[기획] 부동산 가치평가 개혁 골든타임…금융·AVM·정부 간 이해상충 위험,” 2025.12.15

XAI Land is an AVM infrastructure company building an “independent price reference layer” in the Korean residential real estate market. We solve the issues of over- and under-valuation arising from a structure overly reliant on manual appraisals, enabling financial institutions to assess collateral value in a consistent and verifiable manner.

We provide collateral risk management, portfolio monitoring, and market intelligence solutions for financial institutions and government agencies. Based on an architecture aligned with SHAP-based explainability, A–D confidence grading, and MISMO CCS standards, we build systems capable of responding to FSS inspections and AI Basic Act requirements.

Accuracy Disclosure: xai.land/accuracy · Contact: contact@xai.land · Website: xai.land

You Might Like