담보 평가 오차 1%p가 금융 리스크 수천억을 만든다

2025년 5월 연립·다세대 6,000건 실사: 숫자는 작고, 현장 오류는 컸다

< English follows Korean >

지난해 9월, 불과 6개월 전입니다.

국회 정무위원회 포용금융 정책 포럼에서 발표 기회가 생겼고, 자이랜드가 2025년 5월 연립·다세대 거래 6,000건을 대상으로 진행한 실사 백테스트 결과를 가져갔습니다.

슬라이드에 숫자 하나를 크게 올렸습니다. 654.

부동산원테크시세가 추정값을 내놓지 못한 건수입니다. 전체의 11%.

청중 중 한 분이 손을 들었습니다. “그 11%에서 심사 담당자는 어떻게 결정합니까?”

정해진 답이 없었습니다. 직관이거나 거절입니다. 그리고 그 거절 중 일부는 나중에 부실채권(NPL)이 됩니다.

아파트는 쉽습니다. 빌라는 처음부터 다른 문제입니다

아파트 담보물 심사에서 기존 시스템은 잘 작동합니다. 단지 단위로 표준화되어 있고 거래가 많고, 비교 사례가 풍부합니다.

연립·다세대는 다릅니다. 같은 건물이어도 층마다 준공 연도가 다르고 내부 구조가 다릅니다. 마지막 거래가 3년 전인 경우도 흔합니다. 이런 환경에서 자동화 평가 모델은 두 가지 중 하나를 택하게 됩니다. 틀리거나, 포기하거나.

이 자산군이 전세사기와 저축은행 부실채권의 진원지라는 건 이제 알려진 사실입니다. 2022~2023년 전세사기 사태는 우연이 아니었습니다. 담보 평가 체계의 사각지대가 구조적으로 존재했고, 피해는 정확히 그 사각지대에 집중됐습니다.

이건 심사 담당자의 역량 문제가 아닙니다. 숫자가 없으면 판단할 수 없습니다. 숫자를 못 내놓는 건 시스템의 문제입니다.

백테스트는 이렇게 진행했습니다

자이랜드의 정확도 수치는 이론 모델이 아닌 실제 거래 데이터를 기반으로 검증됩니다. 2025년 9월 국회 발표에서 사용한 방법론은 다음 네 단계로 구성됩니다.

1단계 – 실거래가 수집: 국토교통부 실거래가 시스템에서 2025년 5월 연립·다세대 실거래 데이터를 수집합니다. 이것이 평가 정확도를 측정하는 기준값(ground truth)입니다.

2단계 – 기준 시세 수집: 동일 물건에 대해 부동산원테크시세의 하한·상한 평균가(일반가)를 수집합니다.

3단계 – 자이랜드 AVM 평가: 동일 주소·면적 조건으로 자이랜드 AVM 추정값을 생성합니다.

4단계 – MdAPE 산출: 절대 오차율을 계산하고 중앙값을 취해 MdAPE(중앙값 절대 오차율)를 산출합니다. 평균 대신 중앙값을 쓰는 이유: 이상 거래 한 건이 평균을 크게 왜곡할 수 있습니다. 중앙값은 그렇지 않습니다.

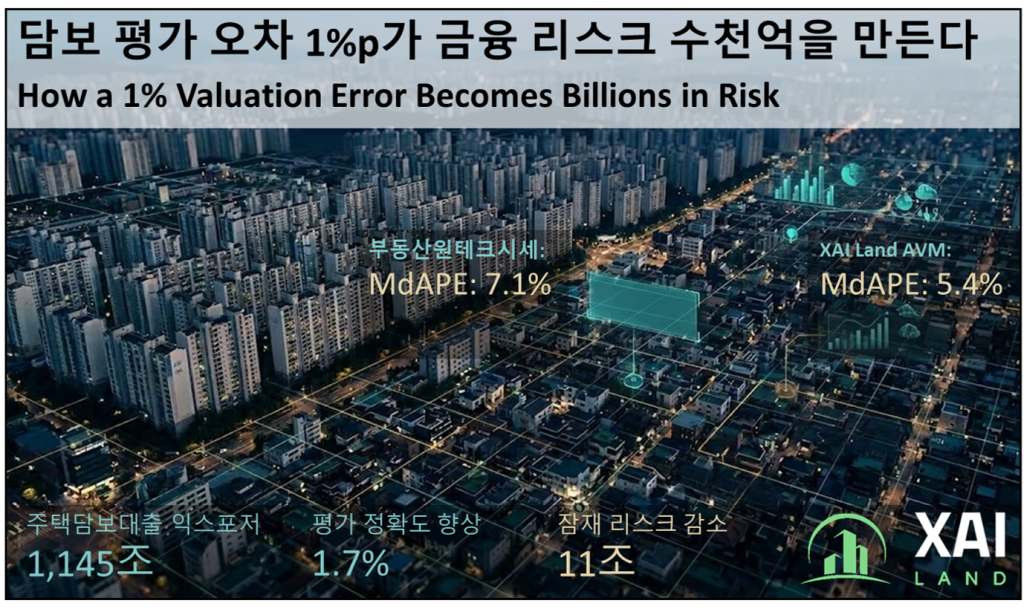

이 방법론으로 6,000건을 분석한 결과입니다(2025년 5월 실거래 기준):

| 평가 방식 | MdAPE |

|---|---|

| 부동산원테크시세 | 7.1% |

| 자이랜드 AVM | 5.4% |

1.7%p 차이입니다. 수치로는 작아 보입니다. 실제 거래를 보면 그렇지 않습니다.

실제 거래 3건

인천 학익동 사례를 보십시오. 실거래가 ₩3,500만 원짜리 물건에 부동산원테크시세가 ₩5,100만 원을 제시했습니다. 오차 45.7%, ₩1,600만 원 과대평가입니다. 이 수치가 담보 심사에 그대로 들어가면 LTV는 왜곡되고, 담보의 실질 가치는 과소평가됩니다. 자이랜드 AVM은 같은 물건을 ₩3,760만 원으로 추정했습니다. 오차 7.4%입니다.

세 사례 모두 서로 다른 지역, 서로 다른 거래 규모입니다. 세 사례 모두 자이랜드 AVM이 실거래가에 더 근접했습니다. 이것이 MdAPE 1.7%p가 현장에서 의미하는 바입니다.

이 격차가 학술 수준에서 왜 의미가 있는가

백테스트 결과(MdAPE 5.4% vs 7.1%)를 ₩300M 물건에 적용하면:

- 부동산원테크시세 MdAPE 7.1% → 추정 오류: ₩21.3M

- 자이랜드 AVM MdAPE 5.4% → 추정 오류: ₩16.2M

- 건당 절감: ₩5.1M

| 기관 | 연간 규모 |

|---|---|

| 한국주택금융공사(HF) | ₩20조 (2026년 정책모기지) |

| 주택도시보증공사(HUG) | ₩1.24조 (전세보증 사고액) |

| 한국토지주택공사(LH) | ₩15조 (연 5만 호 매입 추정) |

| 합계 | ₩36조 |

중규모 저축은행 포트폴리오에서는 1만 건이면 ₩510억, 5만 건이면 ₩2,550억입니다.

예상 손실(EL) 계산과 자본적정성 모델에 직접 반영될 수 있는 수치입니다.

1,148조 원이라는 맥락

2024년 말 기준, 국내 주택담보대출 잔액은 약 1,148조 원입니다.

담보 평가 정확도가 전체 포트폴리오에서 1%p 어긋나 있다면, 시스템이 인식하지 못하는 잠재 리스크는 약 11조 원입니다. 추정이 아닙니다. 산수입니다.

이 수치가 LTV 산정과 자본 요건 계산의 기초가 됩니다.

“왜 이 물건이 이 금액입니까” – 그 질문에 답할 수 있어야 합니다

일부 AVM 기업들은 인터뷰나 언론 기사에서 모델 오차 통계와 같은 요약 지표를 언급하기도 합니다. 그러나 기관이나 일반 대중이 직접 확인할 수 있도록 모델 성능을 웹사이트에 상세히 공개하는 경우는 거의 없습니다.

자이랜드의 접근은 바로 여기에서 시작됩니다. 자이랜드는 모델 정확도 결과를 공개하는 대시보드를 운영하고 있으며, 기관의 리스크 관리에 도움이 되도록 SHAP 기반 설명 가능성 및 신뢰 등급과 같은 기능을 포함한 평가 파이프라인을 구축했습니다.

어떤 AVM이든 MdAPE 수치는 발표할 수 있습니다. 하지만 그것만으로는 충분하지 않습니다.

2026년 1월 시행된 AI 기본법은 대출 심사 AI를 고영향 AI로 분류하고 설명가능성을 의무 요건으로 지정했습니다. 실제 집행은 2027년 초로 예상됩니다. 필요한 인프라가 없다면 준비할 시간은 많지 않습니다.

금융기관의 모델 리스크 심사나 감독기관이 “이 물건이 왜 이 금액으로 평가되었습니까?”라고 질문할 때 단일 지표 하나로는 답이 되지 않습니다. 근거가 필요합니다.

자이랜드의 SHAP 기반 감사 추적은 모든 평가에 대해 어떤 특성이 최종 추정값을 얼마나 움직였는지를 실시간으로 기록합니다. 규제 대응으로 나중에 붙인 기능이 아닙니다. 처음부터 정확도를 증명하는 방법이 감사 추적이었기 때문에 이렇게 설계했습니다.

신뢰 등급(Confidence Grades A~D)은 모델이 해당 물건에 대해 얼마나 확신을 갖는지를 명시합니다. 구축 연도가 오래되고 거래가 희박한 빌라에서는 D등급이 표시됩니다 – 추가 현장 감정을 집중해야 한다는 신호입니다.

SHAP와 신뢰 등급은 정확도의 부산물이 아닙니다. 정확성을 증명하는 근거입니다.

자이랜드는 누구나 무엇을 대체하려는 기술이 아닙니다. 복잡한 물건에는 언제나 현장 전문성이 필요합니다. AVM의 역할은 어떤 물건이 실제로 그 전문성을 필요로 하는지를 정확히 식별하고, 나머지 대부분의 물건을 빠르고 일관되며 투명하게 처리하는 것입니다.

맺으며: 다음 미팅에서 물어보십시오

방향은 이미 정해졌습니다. 문제는 속도입니다.

HF는 AX 전략 2026~2028에서 AVM을 리스크 관리와 전세사기 예방의 핵심 도구로 명시했습니다. HUG의 최인호 사장은 올 초 인터뷰에서 “보증 심사와 리스크 관리 전 과정을 AI 기반으로 재설계하겠다”며 담보 평가 고도화를 AX 전환의 핵심 과제로 꼽았습니다. MG새마을금고중앙회는 2026년 AI 전략부를 신설하고, 연체율 관리를 위한 데이터 기반 여신 심사 고도화에 속도를 내고 있습니다.

세 기관의 공통점은 하나입니다. 담보 평가 정확도가 리스크 관리의 출발점이라는 인식입니다.

다음에 AVM 벤더와 미팅이 있으면 한 가지를 물어보십시오.

“분기별 MdAPE를 지역별, 주택 유형별로 나눠서 공개할 수 있습니까? 실거래가 기준으로요.”

그 대답이 많은 것을 말해줍니다.

참고문헌

- 자이랜드 (2025). “연립·다세대 AVM 정확성 테스팅 방법 및 결과.” 국회 정무위원회 포용금융 포럼 발표자료 (2025년 9월).

- 구강모, 임동준 (2024). “자동가치산정의 정확성 분석 및 투명성 관리 방안.” 부동산분석학회지 (Journal of Real Estate Analysis).

- 한국주택금융공사 (2025). “AX 전략 2026–2028.” HF 내부 전략 문서.

- 주택도시보증공사 (2024). “전세보증 사고 현황.” https://www.khug.or.kr

- 한국은행 (2024). “금융안정보고서 2024년 하반기.” https://www.bok.or.kr

- 금융감독원 (2024). “저축은행 경영 현황.” https://www.fss.or.kr

자이랜드는 한국 주거용 부동산 시장에서 ‘독립적인 가격 참조 레이어’를 구축하는 AVM 인프라 기업입니다. 감정평가 의존 구조에서 발생하는 과대·과소 평가 문제를 해결하고, 금융기관이 담보가치를 일관되고 검증 가능하게 판단할 수 있도록 합니다.

금융기관·정부기관 대상 담보 리스크 관리, 포트폴리오 모니터링, 시장 인텔리전스 솔루션을 제공합니다. SHAP 기반 설명가능성 · A–D 신뢰등급 · MISMO CCS 정합 아키텍처를 기반으로, FSS 검사 및 AI기본법 요건에 대응 가능한 시스템을 구축합니다.

정확도 공시: xai.land/accuracy · 문의: contact@xai.land · 웹사이트: xai.land

How a 1% Valuation Error Becomes Billions in Risk

Backtest across 6,000 multi-unit transactions: the number looks small, the field errors were large

September last year, just six months ago.

XAI Land had a slot at the National Assembly’s Policy Committee financial inclusion forum. We brought the results of a live backtest across 6,000 villa and multi-unit dwelling transactions from May 2025.

One number on one slide. 654.

The cases where Korea Real Estate Board valuations returned no estimate at all. Eleven percent of the total.

A hand went up. “What does the loan officer do in those 11%?”

No clean answer. Intuition, or rejection. And some of those rejections eventually become NPLs (non-performing loans).

Apartments are manageable. Villas are a different problem from the start

Apartment collateral works. Standardized units, high transaction volume, comparable sales everywhere.

Multi-unit villas are different. Different construction years per floor, varying internal layouts, transaction gaps of years. In that environment, automated models do one of two things – guess wrong, or give up.

This asset class is where jeonse fraud and savings bank NPLs concentrate. The 2022–2023 crisis wasn’t random. There was a structural blind spot in the valuation system. The damage went exactly there.

This is not a loan officer competence problem. You cannot make a judgment without a number. When the system can’t produce one, that’s a system failure.

How the backtest was conducted

XAI Land’s accuracy figures are verified against real transaction data. The methodology used in the September 2025 National Assembly presentation follows four steps:

Step 1: Collect MOLIT actual sale transaction data for May 2025 (ground truth).

Step 2: Collect Korea Real Estate Board valuations (부동산원테크시세 lower/upper range average) for the same properties.

Step 3: Generate XAI Land AVM estimates for the same properties at identical address and floor area.

Step 4: Calculate absolute percentage errors and take the median (MdAPE). Median, not mean – a single outlier can move an average dramatically; the median holds steady.

Results across 6,000 transactions:

| Valuation Method | MdAPE |

|---|---|

| Korea Real Estate Board (부동산원테크시세) | 7.1% |

| XAI Land AVM | 5.4% |

Three actual transactions

The Incheon Hagik-dong case: a ₩35M property with a ₩51M REB valuation. A 45.7% overestimate, ₩16M above the actual sale price. If that enters a loan approval process unchallenged, LTV is distorted and the real collateral cushion is overstated. XAI Land’s AVM estimated ₩37.6M – 7.4% error.

Three cases. Three cities. Three price points. In all three, XAI Land was substantially closer to the actual sale price.

Scaled to a portfolio

On a ₩300M property:

- REB MdAPE 7.1% → estimated error: ₩21.3M

- XAI Land AVM MdAPE 5.4% → estimated error: ₩16.2M

- Per-property improvement: ₩5.1M

| Institution | Annual Scale |

|---|---|

| Korea Housing Finance Corp. (HF) | ₩20T (2026 policy mortgage target) |

| Housing & Urban Guarantee Corp. (HUG) | ₩1.24T (annual jeonse guarantee claims) |

| Korea Land & Housing Corp. (LH) | ₩15T (est. 50,000 homes/yr at ₩300M avg) |

Across HF’s 66,000 policy mortgage loans: ₩336.6 billion annually. All three institutions combined: approximately ₩617 billion.

For a mid-sized savings bank with 50,000 loans: ₩255 billion in reduced risk estimation error.

“Why did this property get this valuation?”…you need to be able to answer that

Many AVM providers occasionally share high-level error statistics in interviews or news articles. But very few publish detailed model results openly on their websites where institutions and the public can review them as a starting point.

This is where XAI Land’s work begins. We publish a public dashboard of our model’s accuracy results and have built our valuation pipeline to provide deeper institutional risk insights, including SHAP-based explainability and confidence grading for every property valuation.

Any AVM can publish an MdAPE number, but that alone is not enough.

Korea’s AI Basic Act, in force since January 2026, classifies loan review AI as high-impact and makes explainability mandatory. Enforcement is expected in early 2027. Without the infrastructure, that window closes fast.

XAI Land’s SHAP-based audit trail records, for every valuation, which features moved the estimate and by how much in real time. This was not added later for regulatory compliance. Audit-traceability was how we chose to prove accuracy from the start.

Confidence Grades (A–D) tell the institution exactly how confident the model is about each property. On older villas with thin transaction histories, a D grade appears signaling that field appraisal resources should be concentrated there.

SHAP and Confidence Grades are not byproducts of accuracy. It is the evidence of accuracy.

XAI Land does not replace anyone or anything. Complex properties will always require field expertise. The role of an AVM is to identify which properties truly require that expertise, while processing the remaining majority quickly, consistently, and transparently.

One question for your next meeting

The direction has already been set. The question is pace.

HF’s AX Strategy 2026–2028 names AVM as a core tool for risk management and jeonse fraud prevention. HUG President Choi In-ho stated in a February 2026 interview that the corporation plans to “redesign the entire process of guarantee underwriting and risk management on an AI basis,” with collateral valuation accuracy as a central component. Korean Federation of Community Credit Cooperatives (KFCC) established an AI Strategy Division in 2026 and is accelerating data-driven loan review improvements in direct response to elevated NPL ratios.

The same thesis runs through all three institutions: valuation accuracy is where risk management begins.

When you next meet with an AVM vendor, ask this:

“Can you provide your quarterly MdAPE breakdown by region and property type, based on actual transaction prices?”

That answer tells you most of what you need to know.

References

- XAI Land (2025). “Villa AVM Accuracy Testing.” National Assembly Financial Inclusion Forum (September 2025).

- Koo, Chetti (2024). “An Analysis of the Accuracy of Automated Valuation Model and Transparency Management Plan.” Journal of Real Estate Analysis.

- Korea Housing Finance Corporation (2025). “AX Strategy 2026–2028.”

- HUG (2024). Jeonse Guarantee Claims Statistics. https://www.khug.or.kr

- Bank of Korea (2024). Financial Stability Report H2 2024. https://www.bok.or.kr

- FSS (2024). Savings Bank Management Statistics. https://www.fss.or.kr

XAI Land is an AVM infrastructure company building an “independent price reference layer” in the Korean residential real estate market. We solve the issues of over- and under-valuation arising from a structure overly reliant on manual appraisals, enabling financial institutions to assess collateral value in a consistent and verifiable manner.

We provide collateral risk management, portfolio monitoring, and market intelligence solutions for financial institutions and government agencies. Based on an architecture aligned with SHAP-based explainability, A–D confidence grading, and MISMO CCS standards, we build systems capable of responding to FSS inspections and AI Basic Act requirements.

Accuracy Disclosure: xai.land/accuracy · Contact: contact@xai.land · Website: xai.land

You Might Like