자이랜드의 언더라이팅 AVM: 마케팅 AVM으로 가득한 시장에서의 투명성 필요성

- 마케팅 vs 언더라이팅 AVM – 시장 혼란과 부정확한 감정평가

- 시민 부담 증가 – 부정확한 감정가로 대출 차별 발생

- 투명성 문제 – 마케팅 AVM은 성능 비공개, 언더라이팅 AVM은 공개

- 가계부채 리스크 – 잘못된 감정가가 부채 악화

- 정확한 감정평가 요구 – 금융기관/정부에 투명성 강화 요구

빠르게 진화하는 한국의 부동산 시장에서 정확한 부동산 평가는 은행, 투자자, 주택 구매자 모두의 의사 결정에 중요한 역할을 합니다. 자동가치산정모형(AVM)이 널리 보급되었지만 모든 AVM이 동일한 용도로 사용되는 것은 아닙니다. 현재 시장에 나와 있는 많은 AVM은 마케팅 목적으로 설계되어 정확성을 보장하기보다는 정식 감정평가 서비스, 중개 또는 주택담보대출 서비스로 사용자를 유도하기 위한 추정치를 제공합니다. 반면, 자이랜드의 AVM은 언더라이팅용으로 제작되어 금융 기관과 진지한 투자자가 요구하는 투명성, 정확성, 신뢰성을 제공합니다.

주요 차이점: 마케팅 AVM과 언더라이팅 AVM의 차이점

대부분의 소비자는 모든 AVM이 동일한 수준의 정확도로 부동산 가치를 추정하도록 설계되었다고 생각하지만, 현실은 상당히 다릅니다.

마케팅 AVM: 무료이지만 그 대가는?

- 책임성 부족: 많은 AVM 제공업체는 성능 지표, 샘플 크기 또는 지역별 정확도 분석을 공개하지 않습니다.

- 참여를 유도하기 위한 설계: 많은 마케팅 AVM은 매우 정확한 부동산 가치 평가를 제공하기보다는 사용자의 관심을 끌기 위해 설계되었습니다. 이들은 광범위한 가격 동향과 사용자 생성 입력을 사용하여 낙관적으로 보일 수 있는 추정치를 생성함으로써 플랫폼의 참여도를 높입니다.

- 과대평가 위험: 이러한 AVM은 종종 참여를 우선시하기 때문에 부동산 가치를 과대평가하는 경향이 있으며, 이는 주택 구매자와 대출 기관을 오도하여 금융 리스크로 이어질 수 있습니다. 예를 들어, 2023년 8월 아파트 거래 19,995건을 조사한 결과, 널리 사용되는 마케팅용 AVM이 3,427건에서 10% 이상 가치를 과대평가한 것으로 나타났습니다. 이로 인해 총 1,730억 원이 과대평가되어 금융 의사 결정 및 대출 승인에 영향을 미칠 수 있는 것으로 나타났습니다 (자이랜드 AVM, K*시세·질로우 제쳤다… 정확도 2배 이상 높아).

자이랜드의 언더라이팅 AVM: 정확하고 투명성, 의사결정을 위한 솔루션 구축

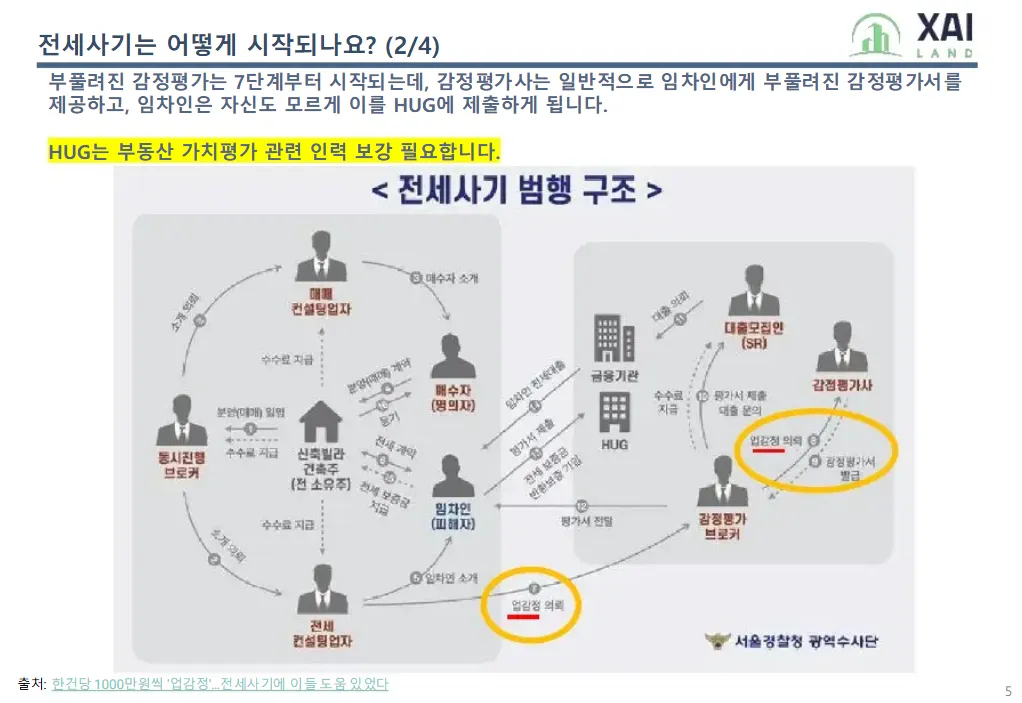

- 국내 AVM 업체 최초로 AVM 정확도 및 투명성에 관한 학술 논문 공동 저자: 언론 인터뷰를 통해 정확도만 발표하는 마케팅용 AVM 업체와 달리, 자이랜드는 AVM 업체 최초로 블로그에 상세한 정확도/오류율 테스트 결과를 공개하기 시작했습니다. 또한 자이랜드는 감정가 부풀리기 및 전세 사기와 관련된 부당 대출 방지와 관련하여 AVM 정확도 및 투명성 방안을 논의한 논문을 발표한 최초의 AVM 업체이기도 합니다 (J. Real Estate Anal.: An Analysis of the Accuracy of Automated Valuation Model and Transparency Management Plan).

- 투명성과 신뢰성과 정확성: 한국의 주거용 부동산에 대한 AVM은 매주 모델을 업데이트하여 85%~95%의 가치 평가가 오차 범위 10% 이내로 유지되도록 지속적으로 개선하고 있습니다 (아파트, 빌라(연립주택/다세대주택), 오피스텔, 단독주택/다가구주택).

- AVM 표준 및 규정을 옹호하는 최초의 AVM 기업: 마케팅 AVM 업체들은 표준 및 규제에 관심이 없는 반면, 자이랜드는 한국에서 AVM의 개발, 사용 및 마케팅 방식을 안내하는 강력한 규제 및 표준을 공개적으로 옹호한 최초의 AVM 업체입니다 (레이, 자이랜드가 이 포럼에 참여했습니다: 그래서 뭐죠?).

- 엄격한 데이터 정리, 처리 및 모델링 인프라: 모든 프롭테크 기업이 동일한 공개 데이터에 액세스할 수 있지만, 부동산 데이터/GIS 분석가가 직접 이끄는 자이랜드의 팀은 ‘더러운’ 공개 데이터를 정리하고 수정하는 가장 포괄적이고 심층적인 데이터 파이프라인 중 하나를 개발했습니다 (자이랜드의 향상된 데이터파이프라인). 자이랜드는 데이터 정리 및 수정 외에도 다른 국내 AVM 서비스에서 확인된 것처럼 방치할 경우 AVM의 정확도에 악영향을 미칠 수 있는 다양한 데이터 관련 문제를 파악할 수 있었습니다.

다른 AVM은 왜 무료인가요? 소비자들이 궁금해해야 할 질문

일반 대중에게 가치 평가에 대한 공개 액세스를 제공하는 마케팅 AVM 제공업체가 자사 모델이 매우 정확하다고 주장한다면, 왜 무료로 부동산 가치 평가를 제공하는 것일까요?

현실적으로 이러한 무료 AVM은 신뢰할 수 있는 평가 도구라기보다는 리드 생성 도구인 경우가 많습니다.

사용자는 무료 AVM의 인센티브가 무엇인지, 그리고 중요한 신용 또는 재무 결정에 진정으로 신뢰할 수 있는지 의문을 가져야 합니다.

귀하의 은행이나 정부 기관에서는 어떤 종류의 평가 서비스를 사용하고 있나요?

주택담보대출을 받거나 정부 주택 기관과 협력하는 경우, 은행이나 기관이 부동산 가치를 결정하는 방식에 의문을 품은 적이 있나요?

많은 금융 기관과 정부 기관에서 AVM을 사용하고 있지만, 모든 AVM이 똑같이 만들어진 것은 아닙니다. 일부는 오래된 모델을 사용하거나, 투명성이 부족하거나, 정확성보다 편의성을 우선시하는 경우도 있습니다. 이는 대출 조건, 주택담보대출 승인, 심지어 주택 정책에도 영향을 미칠 수 있습니다.

소비자는 은행이나 정부 기관이 어떤 부동산 평가 서비스를 사용하고 있는지, 그 서비스가 정말 정확하고 편견 없이 투명하게 정확도/오류율을 보고하는지 문의할 권리가 있습니다.

다음은 가장 정확하고 공정하며 편견 없는 부동산 감정평가 서비스를 제공받고 있는지 확인하기 위해 은행이나 정부 기관(예: HUG, HF 등)에 문의해야 할 몇 가지 질문입니다:

- 기관에서 부동산 가치를 평가할 때 어떤 AVM 또는 평가 방법을 사용하나요?

- 귀사의 AVM은 어떻게 정확성을 보장하며, 공개된 오류율은 얼마인가요?

- 가치 평가 모델이 다양한 가격대 또는 지역에서의 표본 크기 및 정확도와 같은 성과 지표를 공개하나요?

- 성능 및 정확도 메트릭은 어디에서 확인할 수 있나요?

- 실시간 시장 상황을 반영하기 위해 AVM은 얼마나 자주 업데이트되나요?

- AVM이 부동산 가치를 과대평가하거나 과소평가하는 경향이 있나요?

- 재무 리스크로 이어질 수 있는 평가 오류를 방지하기 위해 어떤 안전장치가 마련되어 있나요?

- 차입자 또는 투자자가 AVM 평가에 동의하지 않는 경우, 이를 검토하거나 이의를 제기할 수 있는 절차는 무엇인가요?

- 귀 기관은 정확도 및 지역별 오류율 등 모델 성과 지표를 공개적으로 공유하는 자이랜드와 같은 AVM 제공업체의 사용을 고려하십니까? 그렇지 않다면 현재 사용 중인 AVM의 공개적으로 사용 가능한 성능 데이터를 공유할 수 있나요?

이러한 대화에 참여함으로써 주택 시장을 형성하는 기관에서 투명성을 높이고 더 나은 재무 의사 결정을 내리는 데 도움을 줄 수 있습니다.

주택 가치 평가의 정확성에 관심을 가져야 하는 이유

한국의 은행이나 주택도시보증공사(HUG), 한국주택금융공사(HF) 등 정부 기관이 정확한 주택 가치 평가를 우선시하지 않으면 고객은 심각한 금융 위험에 직면할 수 있으며, 한국 경제는 잘못된 담보 가격과 부풀려진 자산 가치로 인해 가계 부채 증가, 금융 불안 위험 증가, 시장 침체 장기화 등의 문제에 직면할 수 있습니다.

부풀려진 감정평가로 인한 대출자의 금융 부담 증가

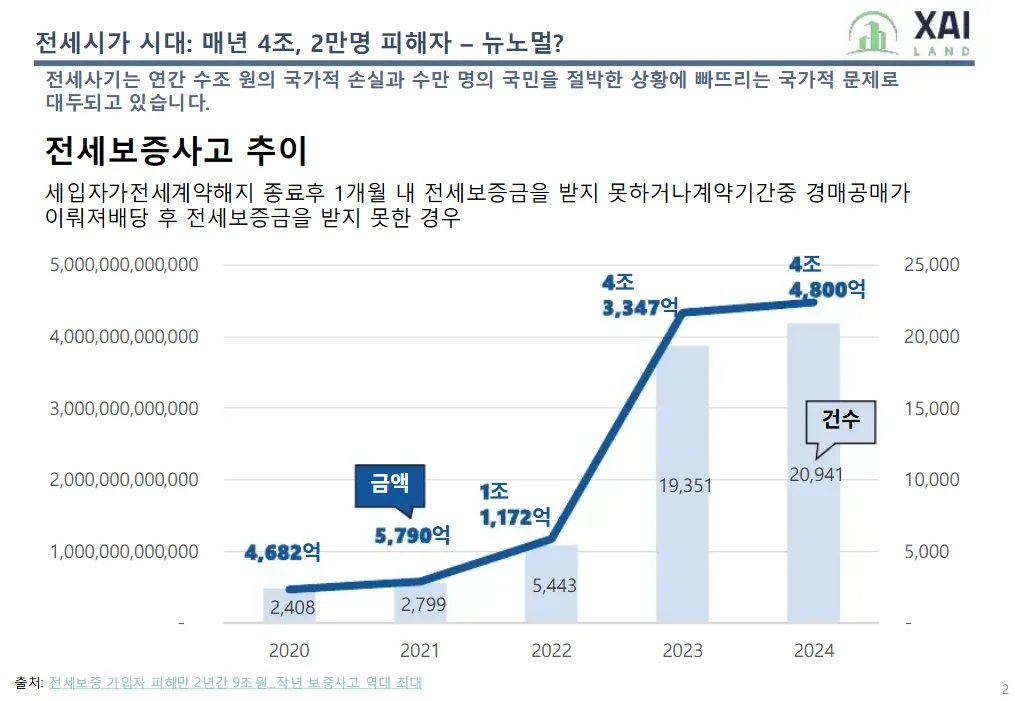

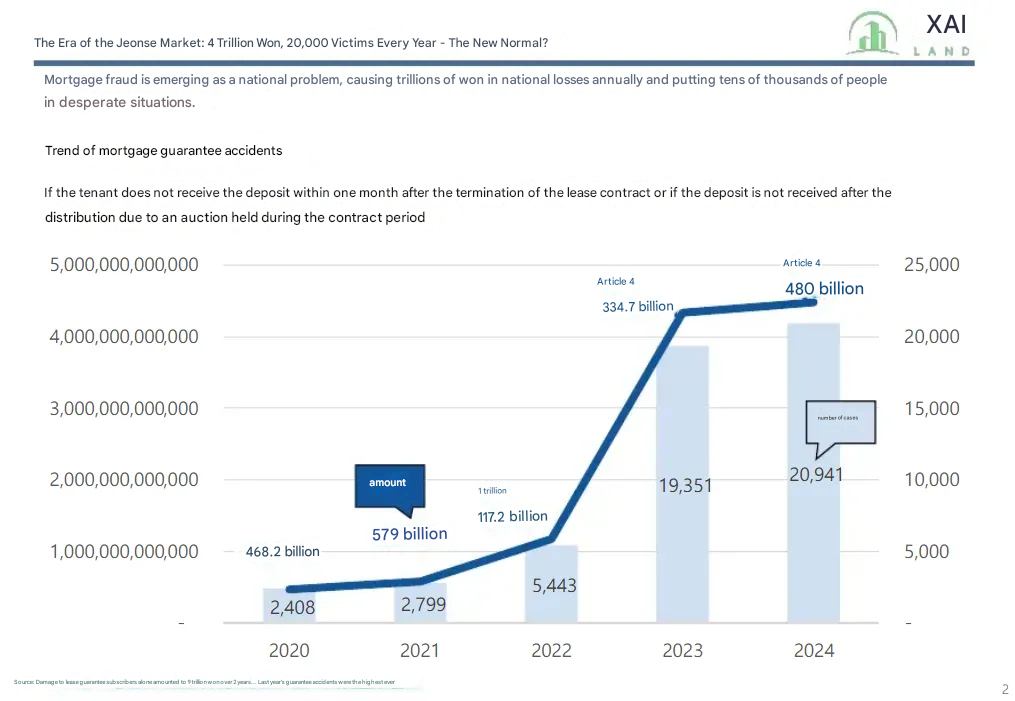

자산 가치가 과대평가되면 대출 금액이 부풀려지거나 전세대출금이 증가하여 대출자의 금융 부담이 커질 수 있습니다. 한국이 경험한 것과 같은 주택 시장 침체가 발생하면 집주인이 전세 보증금을 반환하지 못해 세입자가 상당한 손실을 입을 수 있습니다. 예를 들어, 2024년에는 2만 건이 넘는 전세대출 사기 사건이 신고되었고, 부동산 고평가와 불충분한 안전장치로 인해 총 4조 5,000억원에 달하는 금전적 피해가 발생했습니다.

부정확한 가치 평가로 인한 가계 부채 악화

또한 부정확한 가치 평가는 대출자가 재산 가치보다 더 많은 부채를 떠안게 되어 채무 불이행과 경제 불안정을 초래할 수 있기 때문에 가계 부채 문제를 악화시킬 수 있습니다. 연구에 따르면 한국의 총 가계부채는 약 2,248조 원에 달하며, 이는 3년치 국가 예산을 초과하는 수준입니다. 이러한 규모를 감안할 때, 금융기관과 규제 당국은 차입자의 과도한 레버리지로 인한 위험을 방지하기 위해 정확한 자산 평가를 보장해야 합니다.

유선종 건국대 부동산학과 교수가 강조한 것처럼, 정확한 담보가치 평가는 가계부채 관리에 중요한 역할을 합니다. 특히 현재 대부분의 담보대출 및 여신 관련 의사결정이 이해상충 문제가 있고 과거에 과대평가 및 정확성 문제를 드러낸 감정평가 서비스에 기반하고 있어 객관성, 신뢰성, 정확성에 대한 우려가 제기되고 있는 상황임을 감안할 때, 담보가치 평가의 객관성, 신뢰성, 정확성 제고가 시급합니다.

선종 교수의 논의처럼 금융위원회는 2016년 담합과 감정평가 부풀리기를 방지하기 위해 대출 담당자와 감정평가사를 분리하고 외부 감정평가법인을 무작위로 지정하는 제도를 시행하는 등 국내 부동산 담보대출 관리를 강화하고자 했습니다.

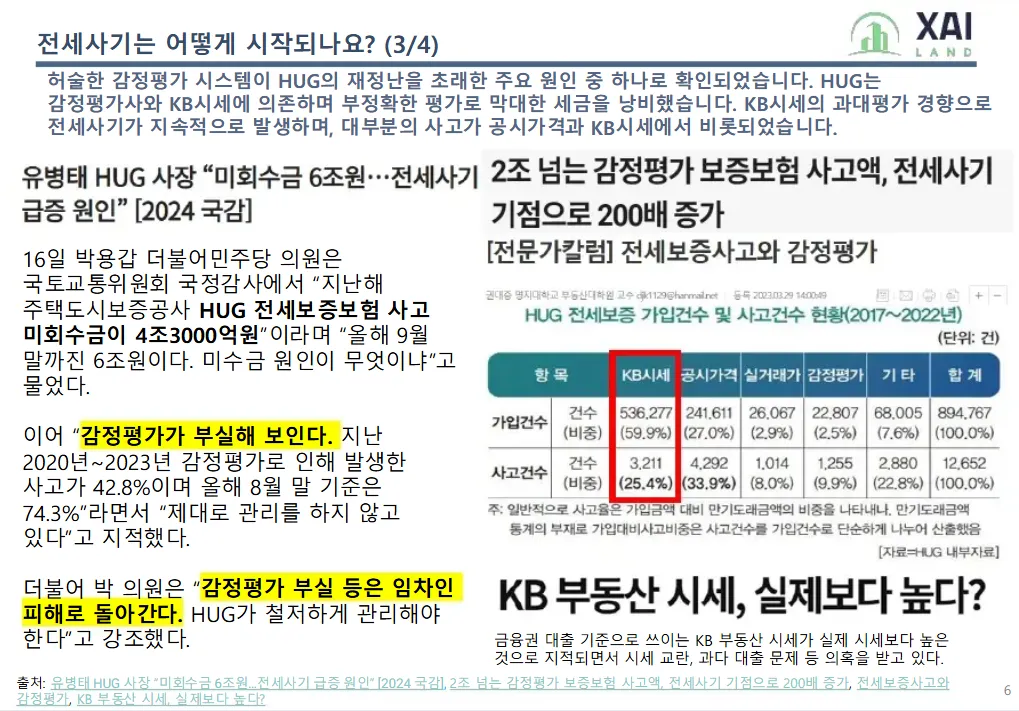

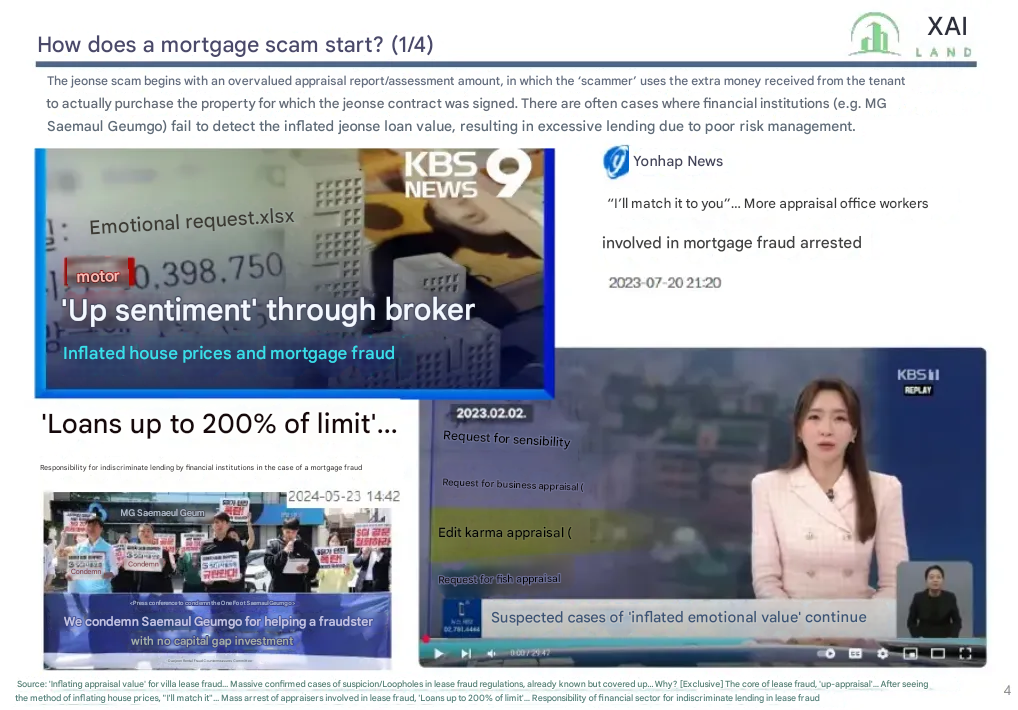

그러나 최근 언론 보도에 따르면 이러한 조치에도 불구하고 유사한 문제가 지속되고 있습니다. 이에 금융감독원은 제출 서류 검증 의무화, 전자 시스템을 통한 감정평가법인 무작위 선정 재도입 등 대출 심사 절차를 강화하기 위한 새로운 FSC 대책을 마련했습니다. 이번 대책은 2024년 우리은행, KB국민은행, NH농협은행 등 주요 은행에서 담보 가치 부풀리기, 사기 대출 등 금융 스캔들이 잇따라 발생한 데 따른 것입니다.

또한, 은행 간 담보가치 평가 방법론의 일관성 부족으로 인해 대출자에게 상당한 금융 리스크가 발생하고 있습니다. 최근 한 보고서에 따르면 동일한 아파트 단지의 감정평가액이 은행에 따라 최대 2억 5,000만원까지 차이가 나며, 이는 주택담보대출 한도에 직접적인 영향을 미치고 더 위험한 대출 행위를 부추긴다는 지적이 제기된 바 있습니다. 한 가지 핵심적인 문제는 KB부동산의 시세 커버리지, 또는 그 부족에서 비롯됩니다.

더 심각한 문제는 KB시세가 신축 아파트의 감정평가 자료를 제공하지 않아 대출자가 주택담보대출을 아예 거절당하는 사례가 발생했다는 점입니다. 2024년 3월 SBS 뉴스 보도에 따르면 ‘새희망홀씨대출’ 등 정부 지원 특별 주택담보대출 프로그램을 신청한 일부 차주들이 아파트 KB시세가 없다는 이유만으로 대출이 거절된 것으로 밝혀졌습니다. 극단적인 경우에는 은행에서 대출 신청을 처리하기 전에 자비로 감정평가사를 직접 고용해 공식적인 감정평가서를 작성하라는 지시를 받기도 했습니다. KB 데이터의 이러한 커버리지 격차는 금융권 전반에 걸쳐 공정하고 일관된 부동산 가치평가를 보장하기 위해 보다 강력하고 표준화된 AVM 규정이 시급히 필요하다는 점을 강조합니다.

감정평가 인플레이션을 해결하기 위한 FSC의 지속적인 노력은 부동산 평가 및 리스크 관리에 대한 지속적인 시스템 개혁의 필요성을 강조합니다.

이러한 금융 함정으로부터 소비자를 보호하고 안정적인 주택 시장을 유지하려면 정확한 부동산 가치 평가가 중요합니다.

한국 부동산 가치 평가의 미래: 참여하기

한국의 부동산 시장이 계속 진화함에 따라 부동산 가치 평가의 투명성은 그 어느 때보다 중요해질 것입니다.

자이랜드는 마케팅보다 정확성을 우선시하는 AVM을 제공함으로써 업계 표준을 정립하기 위해 최선을 다하고 있습니다. 금융 기관, 투자자 및 진지한 구매자는 귀사와 협력하는 금융 기관이 단순한 참여가 아닌 언더라이팅을 위해 구축된 가치 평가 모델을 사용하고 있는지 확인할 것을 권장합니다.

일반 시민 및 금융 소비자

주택 가치 평가의 정확성을 확보하는 것은 재정적 안녕을 보호하는 데 매우 중요합니다. 감정평가 또는 AVM 서비스를 평가할 때 위의 주요 질문 목록을 검토해 보시기 바랍니다. 정보에 입각한 결정은 과대평가된 부동산이나 사기성 대출 관행으로 인한 재정적 손실을 예방하는 데 도움이 될 수 있습니다.

또한, 한국의 민간 시민으로서 집값 사기를 예방하고 공정한 부동산 가치 평가를 촉진하기 위한 활동에 동참하고 싶으신 분들은 금융소비자보호포럼을 주최한 (A) 민병덕 의원, (B) 유동수 의원 중 한 분 또는 두 분께 연락해주시기 바랍니다. 이 게시물에서 자료를 참고하고 연락처를 찾아보세요 (레이, 자이랜드가 이 포럼에 참여했습니다: 그래서 뭐죠?).

여러분의 목소리와 참여는 필요한 개혁을 추진하는 데 도움이 될 수 있습니다.

리스크 또는 주택담보대출 부서의 금융 전문가

주택담보대출, 리스크 관리 또는 금융 감독 분야의 의사 결정권자로서 귀하는 한국 주택 시장의 미래를 형성할 수 있는 힘을 가지고 있습니다. 여러분의 기관이 의존하는 가치 평가는 안정적이고 투명한 시장에 기여할 수도 있고, 다음 주택 버블을 불러일으킬 수도 있습니다. 무분별한 감정평가 인플레이션은 과도한 가계 부채, 대출 채무 불이행, 경제 위기로 이어진다는 것을 역사가 증명하고 있습니다.

자이랜드와 같은 독립적인 데이터 기반 AVM 솔루션을 선택하면 금융 기관은 재무 위험을 줄이고, 대출 성과를 개선하며, 과대평가된 부동산으로부터 소비자를 보호할 수 있습니다. 또 다른 위기로 인해 규제가 강화되기 전에 지금이 바로 가치 평가 제공업체를 재평가해야 할 때입니다.

국회의원 및 규제기관용

한국 부동산 시장은 이해상충을 방지하고 데이터 기반의 공정한 부동산 가치 평가를 보장하기 위한 규제 개혁이 시급히 필요합니다. 지난 2월 7일 국회에서 열린 금융소비자보호포럼에서 자이랜드가 주장한 두 가지 주요 정책 변화를 국회의원들이 검토해 주실 것을 촉구합니다 (레이, 자이랜드가 이 포럼에 참여했습니다: 그래서 뭐죠?)

이러한 개혁을 통해 의원들은 소비자를 보호하고, 금융 안정성을 개선하며, 미래의 부동산 위기를 예방할 수 있습니다.

자이랜드는 이러한 중요한 정책 업데이트를 지원하기 위한 인사이트와 데이터를 제공할 준비가 되어 있습니다.

자이랜드(주)에 대하여

자이랜드는 한국인이 어디에 있든 사기, 불공정 관행, 과다 청구의 위험 없이 완전한 투명성을 바탕으로 안심하고 부동산 금융과 거래를 할 수 있는 세상을 꿈꿉니다.

가장 정확한 자동가치산정모형(AVM)을 통해 부동산 거래를 지원하며, 정확한 가치 평가와 투명한 거래 프로세스를 보장하는 것이 우리의 사명입니다. 우리는 부동산 사기를 예방하고 공정한 가격을 보호하며, 국내외 모든 부동산 관련 과정에서 원활하고 안전한 경험을 제공하기 위해 끊임없이 노력하고 있습니다.

더 자세한 내용을 원한다면, https://xai.land/ 를 방문하거나 LinkedIn ( https://www.linkedin.com/company/18522292/ ) 또는 Facebook ( https://www.facebook.com/xailand/ )의 업데이트를 팔로우하십시오.

주요 요약은 Linktree(https://linktr.ee/xai_land)에서도 한눈에 확인하실 수 있습니다.

XAI Land’s Underwriting AVM: The Need for Transparency in a Market Full of Marketing AVMs

- Marketing vs Underwriting AVM – Market Disruption and Inaccurate Appraisals.

- Increased citizen burden – inaccurate valuations lead to lending discrimination.

- Transparency issues – marketing AVMs hide performance, underwriting AVMs disclose it.

- Household debt risk – inaccurate valuations exacerbate debt.

- Demand for accurate valuations – demand more transparency from financial institutions/government.

In South Korea’s rapidly evolving real estate market, accurate property valuation plays a critical role in decision-making for banks, investors, and homebuyers alike. Automated Valuation Models (AVMs) have become widely available, but not all AVMs serve the same purpose. Many AVMs in the market today are designed for marketing purposes, offering estimates to attract users to certified appraisal, brokerage, or mortgage/loan services rather than ensuring precision. In contrast, XAI Land’s AVM is built for underwriting, offering transparency, accuracy, and reliability that financial institutions and serious investors require.

The Key Difference: Marketing AVM vs. Underwriting AVM

Most consumers assume that all AVMs are designed to estimate property values with the same level of accuracy, but the reality is quite different.

Marketing AVMs: Free, but at What Cost?

- Lack of Accountability: Many AVM providers do not disclose performance metrics, sample sizes, or regional accuracy breakdowns.

- Designed for Engagement: Many marketing AVMs are designed to attract user attention rather than provide highly accurate property valuations. They use broad pricing trends and user-generated inputs to create estimates that may appear optimistic, making their platforms more engaging.

- Overvaluation Risks: Because these AVMs often prioritize engagement, they tend to overestimate property values, which can mislead homebuyers and lenders, leading to financial risks. For example, a study of 19,995 apartment transactions in August 2023 showed that a widely used marketing AVM overestimated values by more than 10% in 3,427 cases. This resulted in a total overvaluation of 173 billion KRW, potentially impacting financial decisions and loan approvals (XAI Land AVM outperforms K*시세·Zillow…More than twice as accurate).

XAI Land’s Underwriting AVM: Accurate and Transparent, and Built for Decision-Making

- First South Korean AVM Firm to Co-Author an Academic Paper on AVM Accuracy & Transparency in Korea: Unlike marketing AVM providers that only announce accuracy rates in media interviews, XAI Land was the the first AVM-firm to begin publishing detailed accuracy/error rate tests on our blog. XAI Land also was the first AVM firm to publish a thesis that discussed AVM accuracy and transparency methods as they related to preventing unfair loans associated with inflated appraisals and Jeonse fraud (J. Real Estate Anal.: An Analysis of the Accuracy of Automated Valuation Model and Transparency Management Plan).

- Transparency, Reliability, and Precision: Our AVM undergoes continuous improvements, with weekly model updates ensuring that 85% to 95% of our AVM-generated valuations for residential real estate in South Korea fall within a 10% margin of error (Apartments, Villas, Officetels, Detached Homes, and Multi-Dwelling Units).

- First AVM firm to Advocate for AVM Standards & Regulations: While marketing AVM firms are not concerned with standards and regulations, XAI Land is the first AVM to publicly advocate for stronger regulations and standards to guide how AVMs are developed, used, and marketed in South Korea (Ray, XAI Land Participated in this Forum: So What?).

- Rigorous Data Cleaning, Processing, and Modeling Infrastructure: While all proptech firms have access to the same publicly available data, XAI Land’s team who is led by a real estate data/GIS analyst himself has developed one of the most comprehensive and in-depth data pipelines that cleans and corrects “dirty” public data (XAI Land’s enhanced Data Pipeline). In addition to cleaning and correcting data, XAI Land has been able to identify various data related issues that could have detrimental impacts on an AVM’s accuracy if left unchecked, as XAI Land has observed in other domestic AVM services.

Why Are Other AVMs Free? The Question Consumers Should Be Asking

If marketing AVM providers who provide the general public open access to their valuations claim their models are highly accurate, why are they giving away property valuations for free?

The reality is that these free AVMs are often a lead-generation tool rather than a trusted valuation instrument.

Users should question the incentives behind free AVMs and whether they can truly be relied upon for critical credit or financial decisions.

What Kind of Valuation Service is Your Bank or Government Agency Using?

If you’re taking out a mortgage or working with a government housing agency, have you ever questioned how your bank or institution determines property values?

Many financial institutions and government agencies rely on AVMs, but not all AVMs are created equal. Some use outdated models, lack transparency, or even prioritize convenience over accuracy. This can impact loan terms, mortgage approvals, and even housing policies.

As a consumer, you have the right to ask your bank or government agency what real estate valuation service they are using and whether it is truly accurate, unbiased, and transparent in reporting it’s accuracy/error rates.

Here are a few questions you should ask your bank or government institution to ensure you’re being offered the most accurate, fair, and unbiased real estate valuation (e.g., HUG, HF, etc):

- What AVM or valuation method does your institution use to assess property values?

- How does your AVM ensure accuracy, and what is its published error rate?

- Does your valuation model disclose performance metrics, such as sample sizes and accuracy at different price points or regions?

- Where can I see their performance and accuracy metrics?

- How often is the AVM updated to reflect real-time market conditions?

- Does the AVM tend to overestimate or underestimate property values?

- What safeguards are in place to prevent valuation errors that could lead to financial risks?

- If a borrower or investor disagrees with an AVM valuation, what is the process for reviewing or challenging it?

- Would your institution consider using an AVM provider like XAI Land, which publicly shares model performance metrics, including accuracy rates and regional error rates? If not, can you share publicly available performance data from the AVM currently in use?

By engaging in these conversations, you can help push for greater transparency and better financial decision-making at the institutions that shape the housing market.

Why Should You Care About the Accuracy of Your Home Valuation?

If South Korea’s banks or government agencies like the Housing and Urban Guarantee Corporation (HUG), Korea Housing Finance Corporation(HF), among others, do not prioritize accurate home valuations, customers may face significant financial risks, and the South Korean economy may face heightened household debt, increased risk of financial instability, and prolonged market downturns due to mispriced collateral and inflated asset values.

Inflated Appraisals lead to Increased Financial Burdens for Borrowers

Overestimated property values can lead to inflated mortgage amounts or larger Jeonse deposits, increasing the financial burden on borrowers. In the event of a housing market downturn, such as the one South Korea experienced, landlords may struggle to return Jeonse deposits, leaving tenants vulnerable to substantial losses.

For instance, in 2024, over 20,000 cases of Jeonse fraud cases were reported, with financial damages totaling almost 4.5 trillion KRW, partly due to overvalued properties and insufficient safeguards.

Inaccurate Valuations lead Exacerbate Household Debt

Additionally, inaccurate valuations can exacerbate household debt issues, as borrowers may take on more debt than their property is worth, leading to potential defaults and broader economic instability. Research has shown that the total household debt in South Korea has reached nearly 2,248 trillion KRW, surpassing three years’ worth of the national budget. Given this scale, financial institutions and regulatory bodies must ensure precise property valuations to prevent the risks associated with overleveraged borrowers.

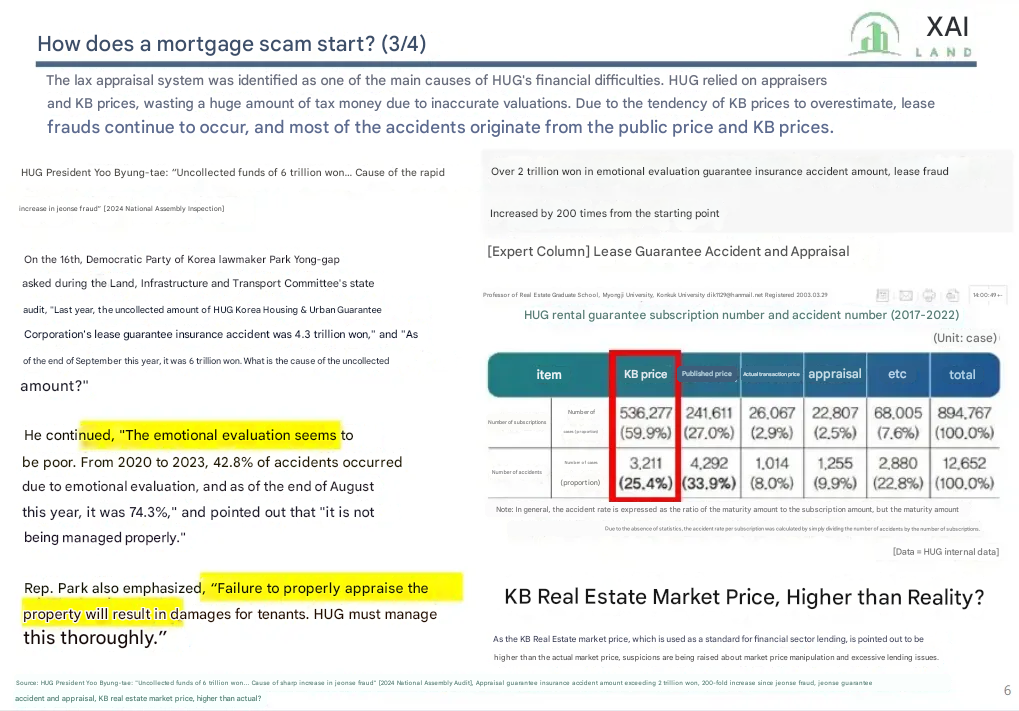

As highlighted by Professor You Seonjong (유선종 건국대 부동산학과 교수), accurate collateral valuation plays a critical role in managing household debt, especially given that most mortgage and credit related decisions are currently based on valuation services that have a conflict of interest issue and have exhibited over-valuation and accuracy issues in the past – raising concerns about objectivity, reliability, and accuracy. Professor Seonjong also discussed how the Financial Services Commission (FSC) sought to strengthen South Korea’s real estate collateral loan management by separating loan officers from appraisal officers and implementing a system that randomly assigned external appraisal firms to prevent collusion and appraisal inflation in 2016.

However, as recent news reports indicate, similar problems persist despite these measures.

A new FSC initiative aims to reinforce loan screening processes, including mandatory verification of submitted documents and reintroducing random selection of appraisal firms through an electronic system. This renewed effort follows a series of financial scandals involving inflated collateral values and fraudulent loans at major banks, including Woori Bank, KB Kookmin Bank, and NH Nonghyup Bank in 2024.

Moreover, the lack of consistency in valuation methodologies across banks has created significant financial risks for borrowers. A recent report highlighted that appraisal values for identical apartment complexes can differ by as much as 250,000,000 KRW depending on the bank, directly impacting mortgage limits and incentivizing riskier borrowing behavior. One key issue stems from KB Real Estate’s market price coverage—or lack thereof.

Worse yet, KB’s failure to provide valuation data for newly constructed apartments has resulted in cases where borrowers were denied mortgage loans altogether. A March 2024 SBS News report revealed that some borrowers applying for government-backed special mortgage programs, such as the Newborn Special Loan (신생아 특례대출), were denied simply because their apartments lacked a KB valuation. In an extreme case, residents were even told to independently hire an appraiser at their own expense to generate an official valuation before the bank would process their loan applications. These coverage gaps in KB’s data highlight the pressing need for more robust and standardized AVM regulations to ensure fair and consistent access to property valuations across the financial sector.

The FSC’s continued struggle to address appraisal inflation highlights the ongoing need for systemic reforms in real estate valuation and risk management.

Ensuring precise property valuations is crucial to protect consumers from these financial pitfalls and to maintain a stable housing market.

The Future of Property Valuation in Korea: Be a Part of It

As South Korea’s real estate market continues to evolve, transparency in property valuation will be more important than ever.

XAI Land is committed to setting the industry standard by providing AVMs that prioritize accuracy over marketing. We encourage financial institutions, investors, and serious buyers to ensure the financial institutions you are working with is using a valuation model built for underwriting – not just engagement.

For Ordinary Citizens & Financial Consumers

Ensuring the accuracy of home valuations is crucial to protecting your financial well-being. We encourage you to review the list of key questions above when evaluating any appraisal or AVM service. An informed decision can help prevent financial loss due to overvalued properties or deceptive lending practices.

Additionally, if you are a private citizen in South Korea who wants to support initiatives to prevent Jeonse fraud and promote fair property valuations, please contact one or both of the representatives who hosted the Financial Consumer Protection Forum – (A) Min Byung-duk and (B) Yoo Dong-soo. Reference the materials and find their contact information in this post (Ray, XAI Land Participated in this Forum: So What?).

Your voice and participation are necessary to help drive needed reforms.

For Financial Professionals in Risk or Mortgage Departments

As a decision-maker in mortgage lending, risk management, or financial oversight, you have the power to shape the future of South Korea’s housing market. The valuations your institution relies on can either contribute to a stable, transparent market or fuel the next housing bubble. History has shown that unchecked appraisal inflation leads to excessive household debt, loan defaults, and economic crises.

By choosing independent, data-driven AVM solutions like XAI Land, your institution can reduce financial risks, improve loan performance, and protect consumers from overvalued properties. Now is the time to reassess your valuation providers—before another crisis forces a regulatory overhaul.

For Lawmakers & Regulators

The South Korean real estate market urgently needs regulatory reform to prevent conflicts of interest and ensure fair, data-driven property valuations. We urge lawmakers to review two key policy changes that XAI Land advocated for at the National Assembly on February 7, 2025 at the Financial Consumer Protection Forum (Ray, XAI Land Participated in this Forum: So What?).

By implementing these reforms, lawmakers can protect consumers, improve financial stability, and prevent future real estate crises. XAI Land is ready to provide insights and data to support these critical policy updates.

About XAI Land

XAI Land envisions a world where Koreans, no matter where they may call home, can confidently finance and transact real estate with complete transparency, free from the risks of fraud, unfair practices, or being ripped off.

Our mission is to support real estate transactions with the most accurate automated valuation models (AVMs), ensuring accurate valuations and transparent transaction processes. We are constantly striving to prevent real estate fraud, protect fair prices, and provide a seamless and secure experience in all real estate-related processes, both domestically and internationally.

For more information, visit https://xai.land/ or follow updates on LinkedIn (https://www.linkedin.com/company/18522292/) or Facebook (https://www.facebook.com/xailand/).

You can also see the main summary at a glance on Linktree (https://linktr.ee/xai_land).

You Might Like