한국에서 자이랜드를 시작하고 운영하는 이유는 무엇인가요?

< English follows Korean >

저는 최근에 사이먼 시넥(Simon Sinek)의 TED 강연을 시청했는데, 그는 1900년대 초반 라이트 형제에게 “패배”한 잘 알려지지 않은 선두주자였던 새뮤얼 피어폰트 랭글리(Samuel Pierpont Langley)에 대한 이야기를 공유했습니다. 이 이야기는 제게 큰 영감을 주었고, 이를 계기로 이 포스트를 작성하게 되었습니다.

이 포스트는 세 부분으로 나누어집니다 – 시작 (2017/18년), 중간 (2019년 및 ‘COVID 시대’), 그리고 현재 (2024년 8월) – 자이랜드의 “왜”가 여러 해 동안 다양한 이해 관계자들과의 대화를 통해 어떻게 진화해왔는지를 설명하고자 합니다.

시작

2017년 후반에 서울에서 6년 반 동안 데이터/GIS 분석가 및 부동산 개발 컨설턴트로 일하면서 부동산 거래를 원활하게 하기 위해 부동산의 가치를 공정하고 편견 없이 평가하는 것이 얼마나 어려우며 비용이 많이 드는지 직접 경험한 후 자이랜드를 설립할 아이디어를 처음 떠올리게 되었습니다.

처음에 저는 한국에는 두 가지 종류의 감정평가가 있다는 것을 알게 되었습니다 – 첫 번째는 ‘탁상자문’으로 불리는 평가로, 주로 엑셀 파일에 근처의 “비교 가능한” 거래 목록과 감정평가사가 부동산의 가치를 어떻게 “생각”했는지에 대한 내용을 포함하고 있었습니다. 이 탁상자문은 무료로 제공되었는데, 처음에는 왜 무료로 제공되는지 의아해했지만, 나중에 알게 된 것은 구매자와 판매자가 엑셀로 작성된 이 “탁상자문”을 검토한 후에는 그 안에 적힌 평가에 대해 “확신”하지 못하게 된다는 것이었습니다.

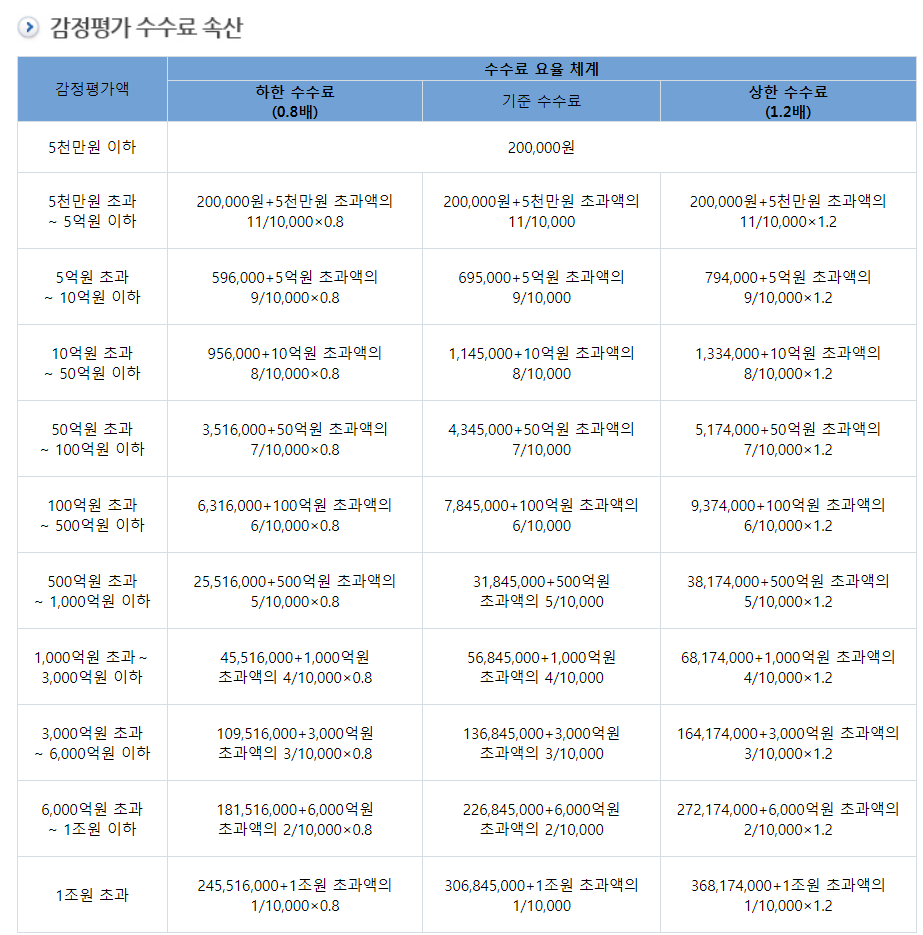

탁상자문의 비효율성을 깨닫고 나서 저는 ‘정식감정’이 무엇인지 배우기 시작했습니다. 이 감정평가는 PDF 형식의 공식 “보고서”로, 부동산의 상태에 대한 감정평가사의 설명과 함께 지도를 포함한 사진과 차트를 포함하고 있었습니다. 제가 문의했던 감정평가의 비용은 약 8백만원에서 3천3백만원원 사이였으며, 이 금액이 감정평가 협회에서 자산의 가격에 따라 정해진다고 하여 매우 놀랐습니다.

당연히, 구매자와 판매자 모두가 이 정도의 비용을 지불할 의향이 없어 감정평가를 받기가 어려웠습니다.

이와 유사한 경험이 반복되면서, 저는 미국의 AVM (Automated Valuation Model, 자동가치산정모형) 회사에서 생성된 AI 가치평가 보고서를 보고 “만약 내가 이 제품을 사용했다면 거래를 성사시킬 수 있었을 텐데!”라고 생각하게 되었습니다.

그 후, 한국의 부동산 데이터에 대한 지식을 바탕으로 많은 연구를 통해 피치덱을 작성하고, Urban Land Institute (ULI) South Korea Young Leaders Group (YLG) 행사를 조직하면서 만났던 감정평가사들을 포함한 부동산 전문가들과 만나게 되었습니다. 이러한 만남을 통해 자신감을 얻게 되었고, 2015년에 설립한 서울영리더스클럽(SYLC)의 친구들에게 연락해 기술 파트너를 찾아 창립 팀을 구성하고 초기 버전의 최소 기능 제품(MVP)을 개발하는 데 도움을 받았습니다.

저는 2018년 3월에 “CRE Korea”(Commercial Real Estate Korea)라는 이름으로 이 ‘아이디어’를 처음 공개했고, 목표는 빅데이터와 AI를 사용해 상업용 부동산을 평가하는 것이었습니다.

모바일에서 보는 경우 Facebook에서 이 게시물을 참조할 수 있습니다.

중간 (Part 1)

회사를 설립한 지 몇 달 후에 프로토타입을 만들었지만, 한 가지 주요 과제가 남아 있었습니다 – 우리는 한국에서 공인된 감정평가 회사가 아닌데 어떻게 AI 기반 감정평가 보고서를 판매할 수 있을까?

이 시점에서 우리는 씨드 투자자인 뉴패러다임 인베스트먼트와 금융위원회의 규제샌드박스에 대해 논의할 기회를 가졌고, 이를 통해 주거용 감정평가 시장이 상업용 부동산 감정평가 시장보다 훨씬 크다는 것을 알게 되었습니다.

모바일에서 보는 경우 Facebook에서 이 게시물을 참조할 수 있습니다.

이들의 통찰력을 바탕으로 우리는 회사를 자이랜드(XAI Land)로 리브랜딩했고, 그 후 자이랜드는 금융위원회의 규제샌드박스에 “혁신금융서비스”로 지정되어 다른 한국 대기업들과 함께 수용되었습니다.

이 시점에서 KB국민은행이 운영하는 KB부동산시세가 부정확하고 과대 평가된 감정평가로 인정을 받기 시작했으며, 여러 주택담보대출 평가 논란이 지속적으로 발생했습니다. 저는 이 기회를 통해 대한민국 부동산 시장에 공정하고 투명한 평가를 도입하여 사람들이 부동산 거래 및 금융을 더 쉽게 할 수 있도록 도울 수 있는 기회를 보았습니다.

저는 KB의 문제를 Zillow가 그들의 Zestimate과 중간 오류율이 약 14%에 달했을 때 받은 비판과 유사한 문제(예: 모델을 만드는 팀에 부동산/데이터 경험이 없는 사람)라고 생각했고, 2016년 한국감정원과 KAIST의 초기 합작사에서 비슷한 시스템을 개발하려다 실패했던 사례가 사이먼 시넥의 강연과 더 관련이 있다고 들었습니다. 결국, 우리는 다른 회사들이 가지고 있지 않은 “왜”를 가지고 있었습니다.

어느 우리 쪽이든, 2018년부터 2020년까지의 초기 성장세를 보면 알 수 있듯이 자금력, 인력, 네트워크가 열세임에도 불구하고 다른 회사에는 없는 ‘이유’가 있다는 것을 알 수 있었습니다.

2020년 하반기에는 한국의 은행 및 감정평가 시장에 대해 연구하고 배운 것이 결실을 맺어 2020년 10월 NH농협은행의 스타트업 협업 및 액셀러레이팅 프로그램인 NH디지털Challenge+에 자이랜드가 합격하면서 ‘왜’가 더 강해졌습니다.

모바일에서 보는 경우 Facebook에서 이 게시물을 참조할 수 있습니다.

중간 (Part 2)에서 현재까지

금융위원회의 규샌드박스에 들어간 지 1년 만에 서울 빌라(연립주택 + 다세대주택)의 AI 가치평가모델을 완성하고, 2021년 5월 OSB저축은행과 함께 성공적으로 테스트를 완료했습니다.

하지만 OSB저축은행과 농협은행과의 대화를 통해 자이랜드가 아직 서비스를 판매할 준비가 되지 않았다는 것을 알게 되었습니다. 잠재 고객들은 다음 두 가지를 원했습니다:

(1) 주거용 주택담보평가에 필요한 모든 것을 제공하는 원스톱 솔루션, 즉, 아파트, 오피스텔, 단독 주택 및 다가구 주택에 대한 AI 평가 모델을 개발하는 것과;

(2) 단순히 숫자 평가에 접근하는 것이 아닌, 실제 평가/감정 보고서와 같은 고품질의 사용자 인터페이스였습니다 (이것이 우리의 2022년 1월 초기 베타 테스트 중 하나에서의 인터페이스였습니다).

2022년은 온갖 감정과 교훈으로 가득 찬 한 해였습니다.

2023년, 부동산 가치 평가에 대한 투명성 부족이 지나치게 부풀려진 평가/감정으로 이어져 전세사기가 시작될 수 있다는 뉴스가 나오기 시작하면서 자이랜드의 ‘이유’가 더욱 강력해졌습니다.

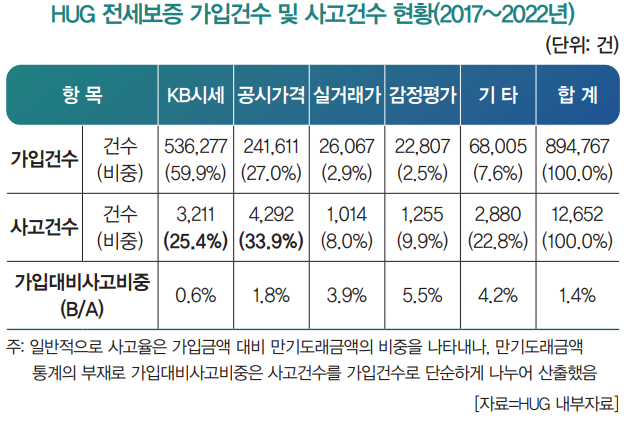

기사에서는 “‘믿을 수 없는 감정가’를 우선 처리하는 ‘감정평가사 보증제도’가 시행된다”는 내용이 자주 언급됐고, KB부동산과 정부 공시가격 등 다른 감정평가 방식이 전체 감정평가 사기 사건의 대부분을 차지한다는 이야기가 나왔습니다. 최근 감정평가법인에 대한 감사 결과, 약 20%의 감정평가법인이 전세사기 행각에 가담하여 부풀려진 감정평가서를 제공한 것으로 나타났습니다.

전세사기를 방지하기 위한 정부의 노력에도 불구하고 전세사기는 계속해서 폭발적으로 증가하고 있습니다.

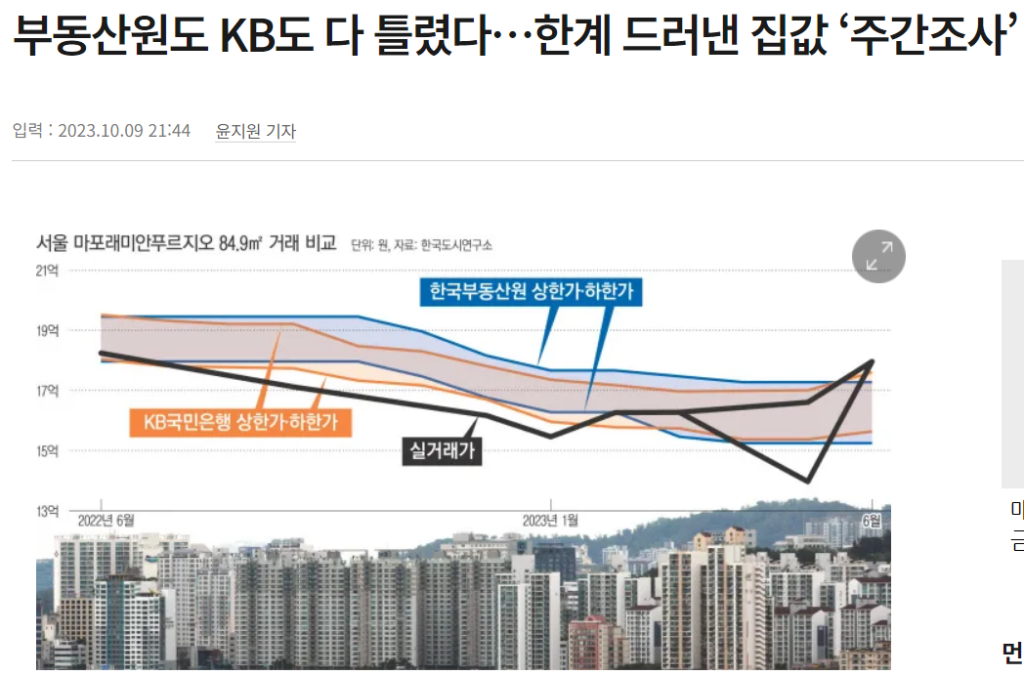

동시에 KB시세과 정부가 운영하는 ‘부동산원’ 플랫폼에 대한 정부 감사에서 두 통계 제공업체가 잘못된 데이터를 제공한 사실이 드러났고, 또 다른 감사에서는 부동산원 담당 공무원이 정치권의 영향을 받아 집값 통계 데이터를 조작한 사실이 드러났습니다.

KB시세의 서비스 문제에 대한 보도가 계속 나오고, 감정가 부풀리기(감정평가 사기)로 인한 금융사고가 급증하면서 국내 은행 및 금융업계가 몸살을 앓고 있는 가운데, 2024년에도 자이랜드의 ‘왜’는 계속 커지고 있습니다:

(1) 2023년 MG새마을금고에서 발생한 은행 대란은 과대 평가 (감정 사기)로 시작되었습니다;

(2) 농협은행에서 64억원(미화 470만 달러) 이상의 재정 비리를 초래한 두 건의 과대 평가 사례 (이 기사가 작성된 시점에서는 NH는 자이랜드의 AVM 솔루션을 사용하지 않고 있습니다) 및;

(3) 여러 은행에서 발생한 124건의 유사한 과대 평가 사례 (감정 사기).

기사에 따르면 “…감정평가의 공정성·독립성을 보장하지 않는 제도의 허점이 금융사고가 반복되는 토양이 됐다고 지적한다.”라고 언급되었습니다.

2024년에도 여전히, 투명하고 정직한 부동산 시장을 육성하고 싶다고 말하는 프롭테크 회사들이 정말로 그렇게 하기를 원하는지 궁금합니다… 특히 자이랜드가 창립 이래로 해오고 있는 것처럼 AVM/AI 모델의 성능을 투명하게 공개하지 않는다면 말입니다. 사실, 저는 얼마 전에도 이 점을 언급했습니다.

자이랜드의 “왜”는 우리 팀이 6년간의 여정 동안 함께 노력하고 배우며 성장하기로 선택하면서 지속적으로 발전해 왔습니다.

상업화로의 “그렇게 선형적이지 않은” 경로에도 불구하고, 나는 2024년 남은 기간 동안 우리가 어떤 기회를 맞이하게 될지에 대해 매우 기대하고 있습니다. 지난달에 6주년 기념 기사를 작성한 이후로 우리에게 찾아온 기회들을 고려할 때 말입니다.

2020년에 상업용 부동산 가치 평가 판매에서 벗어나 주거용 부동산으로 전환하면서 귀중한 기회가 열렸습니다. 이러한 전환이 없었다면 자이랜드는 상업용 부동산 및 토지에 대한 AVM을 안전하고 합법적으로 상용화하는 방법을 배울 기회가 없었을 것이며, FSC 지정 덕분에 만날 수 있었던 다양한 부동산 및 금융 전문가들과 교류하면서 얻은 통찰력을 활용하지도 못했을 것입니다.

이 글을 쓰는 현재 자이랜드는 ‘Value Report’ 제품의 새롭게 개선된 UI/UX를 완성하고 단독주택 및 다가구주택 자동가치산정모형(AVM)을 완성하기 위해 노력하고 있으며, 완료되는 대로 그동안 접촉했던 10여 개의 기관과 다시 협력할 계획입니다.

자이랜드(주)에 대하여

자이랜드는 한국인이 어디에 있든 사기, 불공정 관행, 과다 청구의 위험 없이 완전한 투명성을 바탕으로 안심하고 부동산 금융과 거래를 할 수 있는 세상을 꿈꿉니다.

가장 정확한 AVM을 통해 부동산 거래를 지원하며, 정확한 가치 평가와 투명한 거래 프로세스를 보장하는 것이 우리의 사명입니다. 우리는 부동산 사기를 예방하고 공정한 가격을 보호하며, 국내외 모든 부동산 관련 과정에서 원활하고 안전한 경험을 제공하기 위해 끊임없이 노력하고 있습니다.

더 자세한 내용을 원한다면, https://xai.land/ 를 방문하거나 LinkedIn ( https://www.linkedin.com/company/18522292/ ) 또는 Facebook ( https://www.facebook.com/xailand/ )의 업데이트를 팔로우하십시오.

주요 요약은 Linktree(https://linktr.ee/xai_land)에서도 한눈에 확인하실 수 있습니다.

Why start and run XAI Land in South Korea?

I recently watched Simon Sinek’s TED talk where he shared a story about how the little known, but former front-runner, Samuel Pierpont Langley, “lost” to the likes of The Wright Brothers in the early 1900s, which inspired me to write this post.

This post will be split into three sections – the beginning (2017/18), the middle (2019 & the ‘COVID era’), and now (August 2024) – as XAI Land’s “Why” has constantly evolved given various coffee chats with a variety of diverse stakeholders over the years and various current event.

The Beginning

I originally got the idea to found XAI Land towards the latter half of 2017 after working in Seoul for six and a half years as a data/GIS analyst/real estate development consultant and experiencing exactly how difficult and expensive it was to unbiasedly and fairly value a piece of real estate to facilitate a transaction between a buyer and seller.

At first, I learned how South Korea typically had two versions of appraisals – the first was called a “desktop appraisal” (‘탁상자문’) whose main deliverable to clients involved an Excel file with a list of “comparable” transactions nearby with one cell containing what the appraiser “thought” the property was valued at; these desktop appraisals were free of charge – at first, I was wondering why they were being given to us for free, but I soon found out that as soon as buyers and sellers reviewed these “desktop appraisals” that were done in Excel, neither would be “convinced” about the valuation that was written inside of it.

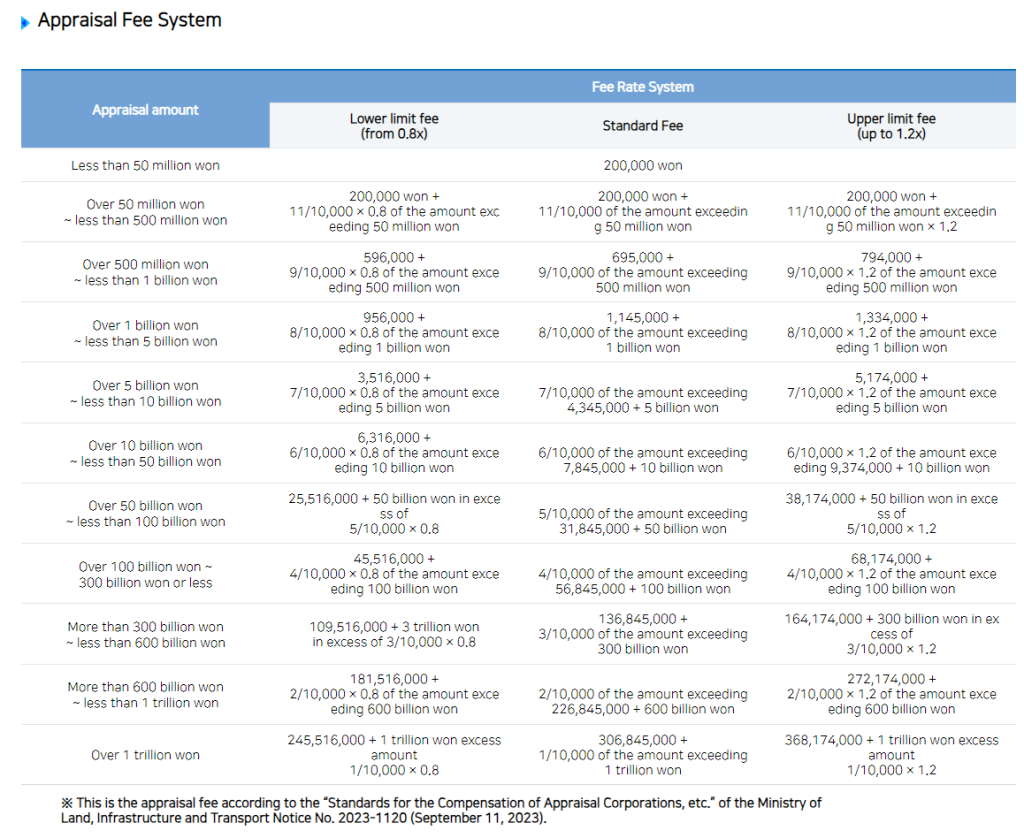

Upon learning the ineffectiveness of desktop appraisals in persuading buyers and sellers about the true value of properties, I then began to learn what a “formal appraisal” (‘정식감정’) was and how these kinds of appraisals included an official “report” typically delivered in PDF format that included maps, charts, and photographs of the property in question with commentary from the appraiser about the condition of the property. Appraisals that I was inquiring for were being quoted at around 8,000,000 KRW to 33,000,000 KRW. I was shocked to learn that the price of “formal appraisals” was regulated by the country’s appraisal association based on how expensive the asset might be as there is no standardized appraisal fee guideline in the US.

Needless to say, it was difficult to get neither party to pay for an appraisal as neither had an interest in spending that much money to value the property.

After similar discussions and experiences happened over and over, I began to think about what was possible after seeing an AI-generated appraisal report from a US-based AVM (Automated Valuation Model) company – after seeing their product I thought to myself…”if only I had that same product when discussing property valuation I definitely could have closed those deals!”

Then, while leaning on my knowledge about Korea’s real estate data, I began putting together a ton of research into a pitch deck and meeting real estate friends and seniors, including appraisers, who I had met thanks to my time volunteering to organize Urban Land Institute (ULI) South Korea Young Leaders Group (YLG) events. It was during these meetings I could gain the confidence I needed to begin reaching out to my friends from the volunteer club I helped found in 2015 called SYLC, Seoul Young Leaders Club, to seek out technology partners who ended up playing various roles in helping create our founding team and helped build the early version of our minimum viable product (MVP).

I first unveiled our ‘idea’ as “CRE Korea” (Commercial Real Estate Korea) in March 2018 where our goal was to value commercial real estate using big data and AI.

The Middle (Part 1)

We built a prototype a few months after incorporating the company, one key challenge remained – how could we sell our AI-based appraisal reports when we were not a certified Korean appraisal company?

It was around this time we had the opportunity to discuss and learn from our seed investors, New Paradigm Investment about the Financial Service Commission’s (FSC) regulatory sandbox and how it might be able to help us expand our target market as we heard the residential appraisal market was much larger than the commercial real estate appraisal market.

With their insight, I embraced a broader approach to our work by renaming our company to XAI Land. Shortly thereafter, XAI Land was successfully designated as an “Innovative Financial Service” and received acceptance to the FSC’s regulatory sandbox alongside other South Korean conglomerates.

It was around this time South Korea’s largest similar player called KB Real Estate operated by Kookmin Bank began getting recognized for inaccurate, over-valued valuations that continually led to various mortgage valuation controversies so I saw this as the perfect opportunity to bring real unbiased and transparent valuations to the South Korean real estate market that would help people transact and finance real estate with ease.

I likened KB’s issues with similar staffing issues (e.g: team making the models didn’t have any real estate/data experience) that plagued Zillow when they were receiving criticism for their Zestimate and median error rates that were clocking in at around 14%, while I heard earlier failed attempts to develop a similar system that were made by the Korea Appraisal Board and KAIST’s early joint venture in 2016 were more so related to Simon Sinek’s talk.

Either way, in my view I knew we had something others did not – the why – despite being out-funded, out-manned, and out-networked – we definitely had “the why” as this was evident in our early traction from 2018 to 2020.

Our “why” became stronger in the latter half of 2020 as our work studying and learning about South Korea’s banking and appraisal market paid off as XAI Land was accepted to Nonghyup Bank’s start-up collaboration and acceleration program, NH Digital Challenge+ in October 2020.

The Middle (Part 2) to Now

In just one year from entering the FSC’s sandbox we completed an AI valuation model for villas in Seoul and successfully tested it with OSB Savings Bank in May 2021.

However, it was through conversations with companies like OSB Savings Bank and Nonghyup Bank, I learned XAI Land could not begin selling subscription fees to our service yet…prospective clients desired two things:

(1) a one-stop valuation shop for their residential mortgage valuation needs, which meant we were being challenged to develop AI valuation models for apartments, officetels, detached homes and multi-family houses in addition to developing;

(2) a much higher quality user interface that functioned like an actual valuation / appraisal report, not just access to our numerical valuations (as this was what our interface was during one of our early beta tests in January 2022).

2022 came and went and was filled with all sorts of emotions and lessons.

2023 saw XAI Land’s “why” grow even stronger as news began to surface about how a lack of transparency over real estate valuations led to over-inflated valuations/appraisals, which was considered the starting point to how Jeonse fraud scams always began.

Articles frequently talked about how “The ‘Jeonse Guarantee System’ that prioritizes the ‘unbelievable appraisers’ will be dealt with” and talked about how other appraisal and valuation methods such as KB Real Estate and the government’s tax assessed valuations composed the majority of all Jeonse fraud cases. A recent audit of appraisal firms found about 20% of them participated in Jeonse fraud schemes and provided inflated appraisals.

Despite government initiatives to prevent Jeonse fraud, Jeonse fraud has continued to explode.

At the same time, government audits of KB Real Estate and the government run “Real Estate One” platform revealed that both statistics providers have provided incorrect data, while another audit revealed government officials in charge of Real Estate One were influenced by politics to manipulate home price statistical data.

XAI Land’s “Why” continues to grow in 2024, as reports continue to emerge on the deficiencies and lack of coverage of KB Real Estate and a sudden spike in financial accidents related to over-inflated appraisals (appraisal fraud) has plagued South Korea’s banking and financial industry:

(2) two instances of inflated appraisals at Nonghyup Bank led to financial misconduct of over 6.4 billion KRW (US$4.7 million) (no, NH is not using XAI Land’s AVM solution as of this article’s writing) and;

Reports have mentioned “…the lack of a system that guarantees the impartiality and independence of appraisals is a recipe for repeated financial failures.”

Even now in 2024, I wonder if proptech companies who say they want to foster a transparent and honest real estate market really mean they want to do this…especially if they are not transparently disclosing their AVM/AI model’s performance in detail as XAI Land has been doing since when it was founded. In fact, I mentioned this not too long ago.

XAI Land’s “why” has constantly been evolving as our team has chosen to persevere, learn, and grow together during the course of our 6 year journey.

Despite our “not-so-linear” path to commercialization, we’re excited about what is to come in the remainder of 2024 given what opportunities have come our way in the past month since I wrote our 6 year anniversary article.

Although XAI Land shifted away from selling commercial real estate valuations in 2020, the FSC designation and pivot to residential properties opened up valuable opportunities – without this shift, XAI Land would not have had the chance to learn how to safely and legally commercialize its AVMs for commercial properties and land, nor would it have benefited from the insights gained through engaging with a wide range of real estate and finance professionals it has been able to meet because of its FSC designation.

As of writing, XAI Land has completed its newly enhanced and revamped UI/UX of our “Value Report” product and is working to complete our AI valuation models (AVMs) for detached homes and multi-family houses, and plans to re-engage with the dozen or so institutions it has had contact with upon completion.

About XAI Land

XAI Land envisions a world where Koreans, no matter where they may call home, can confidently finance and transact real estate with complete transparency, free from the risks of fraud, unfair practices, or being ripped off.

Our mission is to support real estate transactions with the most accurate automated valuation models (AVMs), ensuring accurate valuations and transparent transaction processes. We are constantly striving to prevent real estate fraud, protect fair prices, and provide a seamless and secure experience in all real estate-related processes, both domestically and internationally.

For more information, visit https://xai.land/ or follow updates on LinkedIn (https://www.linkedin.com/company/18522292/) or Facebook (https://www.facebook.com/xailand/).

You can also see the main summary at a glance on Linktree (https://linktr.ee/xai_land).

You Might Like