티몬과 위메프 위기 대응: 자이랜드의 AVM 솔루션이 여신심사 및 리스크관리 팀을 어떻게 지원할 수 있는지

< English follows Korean >

현재 위기 상황: 티몬과 위메프

Qoo10이 소유한 주요 전자상거래 플랫폼인 티몬과 위메프에서 발생한 유동성 문제로 인해 여러 산업에서 상당한 혼란이 발생했습니다. 판매자에 대한 지불 지연으로 인해 주요 소매업체와 서비스 제공업체의 판매가 중단되었고, 이는 더 넓은 경제적 영향을 우려하게 합니다. 이 위기의 파급 효과는 특히 주택 담보 대출 및 포트폴리오 관리 분야에서 금융 부문 전반에 걸쳐 느껴질 가능성이 높습니다.

금융기관의 여신심사 및 리스크 관리에 미치는 영향

은행 또는 주택담보대출 기관에 이 상황은 여러 가지 과제를 제시합니다:

1. 시장 불확실성 증가

- 전자 상거래 부문의 유동성 위기는 시장에 높은 변동성을 초래하여 소비자 신뢰도와 소비 행동에 큰 영향을 미칠 수 있습니다. 소비자들이 더욱 신중해짐에 따라 구매력과 새로운 부채(예: 주택담보대출)를 감수하려는 의지가 감소할 수 있습니다.

- 이러한 불확실성은 차입자의 재정 안정성을 평가하는 데 어려움을 더합니다. 전통적인 신용 평가 모델은 시장 상황의 급격한 변화를 반영하지 못해 차입자의 상환 능력을 오판할 수 있습니다.

- 대출 기관은 실시간 데이터와 시장 동향을 위험 평가 과정에 통합하여 차입자의 재정 행동을 더 잘 예측하고 대응할 필요가 있습니다.

2. 대출 기준 강화

- 위험 환경이 증가함에 따라 금융 기관은 대출 기준을 강화할 수밖에 없습니다. 여기에는 더 엄격한 신용 조사, 더 높은 가치의 담보 요구, 그리고 아마도 더 큰 계약금을 요구하는 것이 포함됩니다.

- 이러한 조치는 기관을 잠재적 손실로부터 보호하려는 목적이지만, 승인 과정이 느려져 신규 대출의 양이 감소하고 일부 고객을 소외시킬 수 있습니다.

- 또한, 더 높은 가치의 담보 요구는 정확한 부동산 평가에 압력을 가합니다. 과대평가는 차입자가 디폴트할 경우 담보가 충분하지 않게 만들고, 과소평가는 신용을 받을 자격이 있는 차입자가 거절당할 수 있습니다. 따라서 이러한 맥락에서 정밀한 부동산 평가 도구인 AVM(자동가치산정모형)이 필수적입니다.

3. 기존 포트폴리오의 모니터링 강화

- 티몬과 위메프와 관련된 비즈니스의 금융 불안정성은 현재의 주택담보대출 포트폴리오를 더 면밀히 검토해야 할 필요성을 강조합니다. 대출 기관은 이러한 비즈니스와 관련된 대출이나 위기 영향을 크게 받는 지역의 대출을 식별해야 합니다.

- 모니터링 강화를 위해 부동산 가치와 차입자의 신용도를 자주 재평가하여 잠재적 디폴트 징후를 조기에 감지해야 합니다. 이러한 사전 예방적 접근은 대출 재구조화 또는 위험에 처한 차입자에게 목표 지원을 제공하는 등의 완화 전략을 실행함으로써 더 큰 손실을 방지할 수 있습니다.

- 개별 대출과 관련된 위험을 신속하고 정확하게 재평가하는 능력은 주택담보대출 포트폴리오의 전반적인 건강을 유지하는 데 도움이 되며, 잠재적인 문제가 확산되기 전에 해결할 수 있습니다.

AVM 솔루션이 도움을 줄 수 있는 방법

이러한 불안정한 시기에 신뢰할 수 있는 AVM 솔루션을 갖추는 것은 매우 중요합니다. 이는 정확하고 시기 적절한 부동산 평가를 지원할 뿐만 아니라 위험 평가와 사전 포트폴리오 관리를 강화하여 금융 기관이 시장의 불확실성을 더 효과적으로 극복할 수 있도록 도와줍니다.

1. 정확하고 시기적절한 부동산 감정

- AVM은 실시간 시장 데이터를 통합하여 최신 부동산 감정을 제공함으로써 담보 평가가 현재 시장 상황을 반영하도록 보장합니다.

- 부동산 특성과 시장 동향에 대한 세분화된 분석을 통해 신용 평가의 정확성을 높입니다.

2. 고급 리스크 평가

- AVM 솔루션은 예측 분석을 사용하여 미래의 부동산 가치와 시장 동향을 예측하고 조기에 잠재적 리스크를 식별할 수 있도록 도와줍니다.

3. 적극적인 포트폴리오 관리

- 주택담보대출 포트폴리오의 지속적인 모니터링을 통해 가치 하락 위험이 있는 부동산을 조기에 감지할 수 있습니다.

- 실시간 경고와 자세한 리스크 평가를 통해 잠재적 손실을 완화하기 위한 적극적인 관리와 신속한 개입을 지원합니다.

4. 차입자 지원 및 디폴트 감소

- AVM이 생성한 개별화된 주택담보대출/평가 리스크 프로필을 통해 리스크가 높은 차입자를 위한 대출 구조 조정이나 상환 계획과 같은 맞춤형 지원 프로그램을 제공합니다.

- 투명하고 신뢰할 수 있는 부동산 감정을 제공하여 차입자, 투자자 및 규제 당국과의 신뢰를 구축하고 귀 기관의 평판과 고객 신뢰를 높입니다.

AVM 솔루션을 채택하지 않을 경우의 결과

시장 불확실성 시기에 자이랜드와 같은 AVM 솔루션을 도입하지 않으면 은행은 상당한 재정적 손실을 입을 수 있습니다.

역사적으로 경제 불안 시기에 부정확한 부동산 평가로 인해 대출 기관의 채무 불이행률이 증가하고 상당한 재정 손실이 발생했습니다. 예를 들어, 2008년 금융 위기 동안 많은 은행이 고평가된 부동산 담보로 인해 심각한 손실을 입었고, 그 결과 채무 불이행률이 높아지고 자산 가치가 감소했습니다.

미국 연방주택금융청의 정책 분석 및 연구실과 조지 워싱턴 대학교 경제학과 연구진이 작성한 “주택 가격 인상과 주택담보대출 채무 불이행“과 같은 최근 연구에 따르면 대침체기에 전통적인 감정 대신 AVM을 활용했다면 많은 담보 위험 기반 채무 불이행을 피할 수 있었을 것이라고 합니다. AVM은 기존 감정평가가 놓칠 수 있는 주택의 기본 가치의 중요한 변화를 포착하여 더 나은 정보에 입각한 대출 결정을 내릴 수 있기 때문입니다. 따라서 주택담보대출 인수 프로세스에 AVM을 통합하면 담보 평가의 정확성을 높이고 잠재적으로 채무 불이행률을 줄일 수 있습니다.

또한, 주택담보대출 포트폴리오를 선제적으로 관리하고 모니터링하지 못하면 조기 개입의 기회를 놓쳐 잠재적인 손실이 악화될 수 있습니다.

AVM 솔루션 도입의 이점

반면에 AVM 솔루션을 통합하면 위험 평가를 강화하고 채무 불이행률을 줄이며 신용 평가 프로세스의 전반적인 효율성을 개선하여 은행에 수백만 달러를 절약할 수 있습니다.

예를 들어, Freddie Mac의 Automated Collateral Evaluation (ACE) 프로그램은 AVM이 신용 위험을 효과적으로 줄일 수 있는 좋은 예를 제공합니다. 프레디맥(Freddie Mac)은 적격 주택담보대출에 대해 전통적인 감정 평가 과정을 면제함으로써 디폴트율을 눈에 띄게 낮추었습니다.

구체적으로, 한 연구에 따르면 ACE 프로그램을 통해 생성된 대출은 평가가 필요한 유사한 대출에 비해 연체율이 약 8.9% 낮았습니다. COVID-19에 대한 지원금 관련 연체를 제외하면, 연체율은 13.9%까지 더욱 낮아집니다. 이와 같은 디폴트율 감소는 Freddie Mac, 투자자 및 주택담보대출 보험사에 상당한 비용 절감으로 이어지며, 주택담보대출 창출 과정의 신속한 대출 종료 및 효율성 개선도 제공합니다

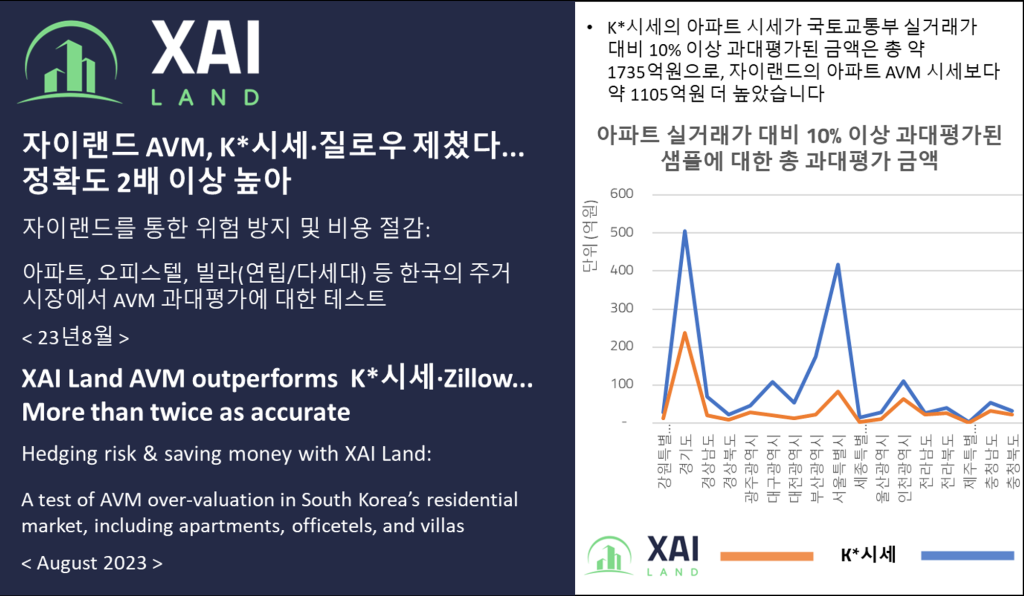

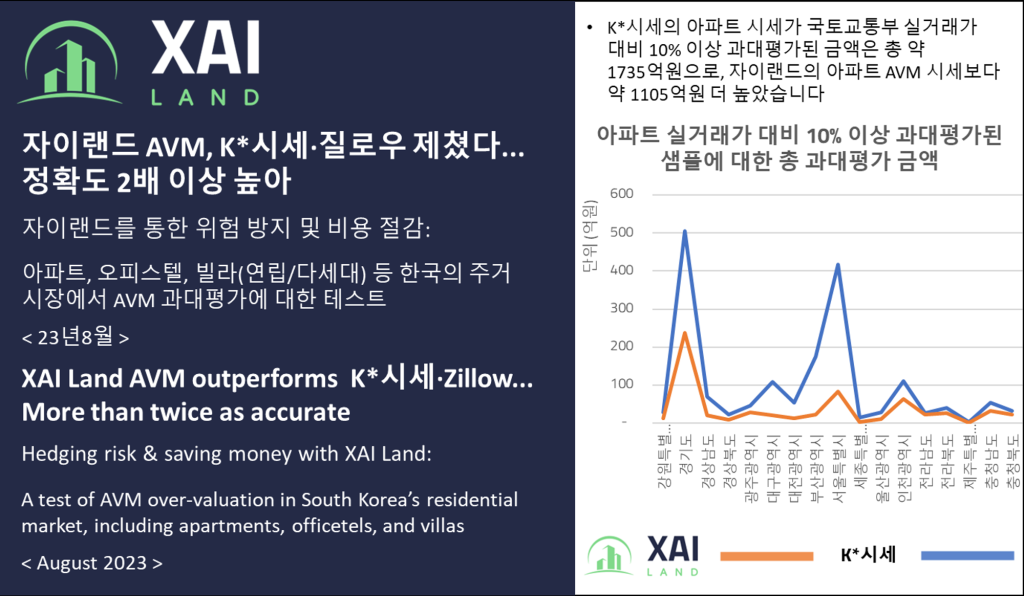

자이랜드의 AVM 솔루션이 한국에서 비교되는 방식

K*시세, 질로우(미국)와 같은 다른 시스템은 일반적인 시장 추정치를 제공하는 반면, 자이랜드의 AVM은 보다 강력한 데이터 파이프라인을 활용하여 필터링되지 않은 원시 데이터와 향상된 모델링 기술을 더 잘 처리하여 더욱 정확한 가치 평가를 제공합니다. 이러한 높은 수준의 정확도는 고평가 또는 저평가의 위험을 크게 줄여 부도율을 낮일 수 있습니다.

한 달 동안 수만 건의 거래를 대상으로 한 연구에 따르면, 자이랜드의 AVM은 다른 시스템보다 두 배 이상의 정확도를 보여 신용 평가 및 리스크 관리 팀에 더욱 신뢰할 수 있는 도구를 제공했습니다.

자이랜드는 2개월 단위로 유사한 벤치마크 테스트를 실시하며 이러한 결과의 일관성을 확인할 수 있습니다.

은행은 자이랜드의 AVM 솔루션을 프런트엔드 평가 보고서 또는 RestAPI 솔루션으로 활용함으로써 주택담보대출 포트폴리오를 더 잘 관리하고, 상당한 재정 손실을 방지하며, 변동성이 큰 시장에서 더 큰 안정성을 달성할 수 있습니다.

결론

티몬과 위메프의 현재 위기는 주택담보대출 대출에서 강력한 리스크 관리와 정확한 부동산 감정의 중요성을 강조합니다. 자이랜드의 AVM 솔루션은 여신심사 및 리스크관리 팀이 이 어려운 환경을 탐색하는 데 필요한 도구를 제공하여 정보에 입각한 의사 결정, 적극적인 포트폴리오 관리 및 차입자에 대한 지속적인 지원을 보장합니다.

자이랜드의 향상된 AVM 솔루션을 원시 데이터/RestAPI 또는 평가 보고서 형식으로 테스트하여 실험 결과를 확인하고자 하거나 자체 내부 테스트를 희망하시는 경우, 귀하의 신상 정보와 회사 정보, 희망하는 테스트 일정 등을 contact@xai.land로 보내주시기 바랍니다.

Navigating the TMON and WeMakePrice Crisis: How XAI Land’s AVM Solution Can Support Credit Evaluation and Risk Management

The Current Crisis: TMON and WeMakePrice

Recent liquidity issues at TMON and WeMakePrice, prominent e-commerce platforms owned by Qoo10, have caused significant disruptions across various sectors. Payment delays to sellers have led to the suspension of sales by major retailers and service providers, raising concerns about broader economic impacts. The ripple effect of this crisis is likely to be felt across the financial sector, particularly in mortgage lending and portfolio management.

Impact on Credit Evaluation and Risk Management for Financial Institutions

Mortgage providers and lenders face several challenges:

1. Increased Market Uncertainty

- The liquidity crisis in the e-commerce sector introduces a high degree of volatility into the market, which can significantly affect consumer confidence and spending behavior. As consumers become more cautious, their purchasing power and willingness to take on new debt, including mortgages, may decrease.

- This uncertainty complicates the evaluation of borrowers’ financial stability. Traditional credit assessment models may not account for the rapid changes in market conditions, leading to potential misjudgments in the borrower’s ability to repay.

- Lenders need to adapt to these fluctuating conditions by incorporating real-time data and market trends into their risk assessment processes to better predict and respond to borrowers’ financial behaviors.

2. Tighter Lending Standards

- In response to the heightened risk environment, financial institutions may be compelled to tighten their lending criteria. This includes requiring more stringent credit checks, higher-value collateral, and possibly larger down payments from borrowers.

- These measures aim to safeguard the institution from potential losses but could result in a slower approval process, reducing the volume of new loans and potentially alienating some customers.

- Additionally, the need for higher-value collateral places pressure on accurate property valuations. Overvaluation can lead to insufficient collateral in case of borrower default, while undervaluation can cause worthy borrowers to be denied credit. Therefore, precise property valuation tools like AVMs (Automated Valuation Models) become essential in this context.

3. Enhanced Monitoring of Existing Portfolios

- The financial instability of businesses linked to TMON and WeMakePrice necessitates closer scrutiny of current mortgage portfolios. Lenders must identify loans associated with these businesses or those in regions significantly impacted by the crisis.

- Enhanced monitoring involves frequent re-evaluation of property values and borrower creditworthiness to detect early signs of potential default. This proactive approach allows lenders to implement mitigation strategies, such as restructuring loans or providing targeted support to at-risk borrowers, thereby preventing larger losses.

- The ability to quickly and accurately reassess the risk associated with individual loans helps in maintaining the overall health of the mortgage portfolio, ensuring that potential issues are addressed before they escalate.

How AVM Solution Can Help

In these turbulent times, having a reliable AVM solution is crucial. It not only supports accurate and timely property valuations but also enhances risk assessment and proactive portfolio management, enabling financial institutions to navigate market uncertainties more effectively.

1. Accurate and Timely Property Valuations

- AVMs integrate real-time market data to provide up-to-date property valuations, ensuring that collateral assessments reflect current market conditions.

- Granular analysis of property features and market trends enhances the accuracy of credit evaluations.

2. Advanced Risk Assessment

- AVM solutions employ predictive analytics to forecast future property values and market trends, helping identify potential risks early.

3. Proactive Portfolio Management

- Continuous monitoring of the mortgage portfolio enables early detection of properties at risk of devaluation.

- Real-time alerts and detailed risk assessments support proactive management and timely intervention to mitigate potential losses.

4. Supporting Borrowers and Reducing Defaults

- Individualized risk profiles of mortgages (mortgage valuations) generated by AVMs help tailor support programs for at-risk borrowers, such as loan restructuring or repayment plans.

- Providing transparent and reliable property valuations builds trust with borrowers, investors, and regulators, enhancing your institution’s reputation and customer confidence.

Consequences of Not Adopting an AVM Solution

Failing to adopt an AVM solution in times of market uncertainty can lead to significant financial losses for banks.

Historically, during periods of economic instability, inaccurate property valuations have contributed to increased default rates and substantial financial losses for lenders. For example, during the 2008 financial crisis, many banks faced severe losses due to overvalued real estate collateral, which resulted in higher default rates and diminished asset values.

Recent studies such as “House Price Markups and Mortgage Defaults” written by researchers from both the US Federal Housing Finance Agency’s Office of Policy Analysis & Research and George Washington University’s Department of Economics suggest if AVMs had been utilized instead of traditional appraisals during the Great Recession, many collateral-risk-based defaults could have been avoided. This is because AVMs capture important variations in the fundamental value of homes that traditional appraisals may miss, leading to better-informed lending decisions . Thus, incorporating AVMs into the mortgage underwriting process can enhance the accuracy of collateral assessments and potentially reduce default rates.

Moreover, the inability to proactively manage and monitor the mortgage portfolio can lead to missed opportunities for early intervention, exacerbating potential losses.

Benefits of Adopting an AVM Solution

On the other hand, integrating an AVM solution can save banks millions by enhancing risk assessment, reducing default rates, and improving the overall efficiency of the credit evaluation process.

For instance, Freddie Mac’s Automated Collateral Evaluation (ACE) program provides a compelling example of how AVMs can effectively reduce credit risk. By waiving the traditional appraisal process for eligible mortgages, Freddie Mac has achieved a notable reduction in default rates. Specifically, a study found that loans originated through the ACE program have about an 8.9% lower delinquency rate compared to similar loans requiring appraisals. When excluding delinquencies related to COVID-19 forbearance, the default rate drops even further, to 13.9%. This reduction in default rates translates into significant cost savings for Freddie Mac, investors, and mortgage insurers, while also providing faster loan closures and efficiency improvements in the mortgage origination process

How XAI Land’s AVM solution compares in South Korea

While other systems, such as K*시세 and Zillow, provide general market estimates, XAI Land’s AVM leverages more robust data pipelines to better process unfiltered/raw data and enhanced modelling techniques to deliver more precise valuations. This high level of accuracy significantly reduces the risk of overvaluation or undervaluation, which can lead to lower default rates.

According to a study that included tens of thousands of transactions that took place over a month period, XAI Land’s AVM has shown more than twice the accuracy of these other systems, thereby providing a more dependable tool for credit evaluation and risk management teams.

XAI Land conducts similar benchmark tests on a bi-monthly basis and can confirm consistency in these results.

By utilizing XAI Land’s AVM solution either as a front-end valuation report or RestAPI solution, banks can better manage their mortgage portfolios, avoid significant financial losses, and achieve greater stability in volatile markets.

Conclusion

The current crisis at TMON and WeMakePrice underscores the importance of robust risk management and accurate property valuations in mortgage lending. XAI Land’s AVM solution equips credit evaluation and risk management teams with the tools they need to navigate this challenging environment, ensuring informed decision-making, proactive portfolio management, and continued support for your borrowers.

If you may wish to test XAI Land’s enhanced AVM solution (RestAPI) to verify our results or to conduct your own internal testing, please email XAI Land at (contact@xai.land) with a brief explanation of who you are, your organization, and when you may wish to test XAI Land’s AVM solution.

You Might Like