왜 독립형 AVM이 한국의 포용금융에 필수적인가: 국회 발표 후기

< English follows Korean >

2025년 9월 26일, 저는 국회에서 열린 「포용금융 3.0시대 : 금융소외자를 위한 포용금융 방향과 실천전략」포럼에서 발표자로 초청받아 연단에 섰습니다. 이 포럼은 더불어민주당 민병덕 의원, 유동수 의원, 이강일 의원실이 주최하고, 금융과행복네트워크, 시니어금융교육협의회, 한국금융복지정책연구소가 공동 주관했습니다.

금융위원회(FSC), 금융감독원(FSS) 관계자, 은행 및 금융 유관기관 임원, 시민단체 대표 등도 한자리에 모여 한국 금융시스템을 더 포용적이고 더 탄력적으로 만들 방법을 논의했습니다.

저는 사례발표자로서「포용형 담보평가 3.0: 독립형 AVM을으로 여는 지역활성화」을 주제로 한국 주택금융과 담보평가의 미래를 말씀드렸습니다.

제가 전하고자 한 핵심 메시지는 단순했습니다.

투명하고 독립적이며 공정한 담보평가가 없다면, 한국은 진정한 포용금융을 달성할 수 없으며, 감정평가 관련 금융사고와 전세사기 위험에도 여전히 취약하다 (저는 2025년 2월에 국회에 AVM이 어떻게 전세사기를 방지할 수 있는지에 대해 발표할 수 있는 영광을 누렸습니다.).

이 블로그에는 제가 국회에서 발표한 전체 자료를 공개합니다. 누구든지 저희가 주장한 내용과 연구 근거를 직접 확인하실 수 있습니다.

제가 전한 메시지

현 제도의 문제점

- 한국의 담보평가 시스템은 아파트 중심의 시세지수와 주관적 감정평가에 의존하고 있습니다. 이는 청년, 고령층, 저소득 가구가 주로 거주하는 빌라·단독·지역주택을 제도권 밖으로 밀어내고 있습니다.

- 고령층은 단독·빌라 주택이면 주택연금 가입이 막히거나 공시가격 탓에 연금 수령액이 줄어듭니다.

- 황인도 한국은행 연구실장도 “이 조건이 민간 역모기지 확대의 걸림돌”이라고 지적했습니다 (12억 넘어도 가능한 ‘주택연금’이라더니 “아파트만” 가입… “단계적 확대 검토”).

- 황인도 한국은행 연구실장도 “이 조건이 민간 역모기지 확대의 걸림돌”이라고 지적했습니다 (12억 넘어도 가능한 ‘주택연금’이라더니 “아파트만” 가입… “단계적 확대 검토”).

- 청년·무주택자는 KB시세와 감정평가가 실제보다 높게 잡히면서 깡통전세·전세사기로 이어집니다. 전세 제도에 대한 신뢰가 무너지자 수요가 반전세·월세로 몰리고, 공급은 그대로여서 월세 부담만 커집니다. 결국 서민들의 주거 사다리가 끊어지는 악순환이 발생합니다 (“KB시세는 호가에 불과”…HUG 전세보증 사고 터지는 진짜 이유, 부동산원도 KB도 다 틀렸다…한계 드러낸 집값 ‘주간조사’, 자이랜드 AVM, K*시세·질로우 제쳤다… 정확도 2배 이상 높아, KB 부동산 시세, 실제보다 높다?, 서민들 “평생 월세만 살라는 소리” 울분 … 주거사다리 걷어찬 ‘전세보증 70%’).

- 사실 국회에서는 미처 언급하지 못했지만, HUG(주택도시보증공사)와 HF(한국주택금융공사)가 깡통전세 방지를 위해 보증 강화와 LTV 축소 정책을 내놓고 있습니다. 하지만 최근 보고서에서 지적하듯, 이는 오히려 세입자를 반전세·월세로 내몰고 있습니다. 마찬가지로 에스크로 제도도 보호 장치처럼 들리지만, 오히려 월세화를 가속할 수 있다는 전문가 경고가 있습니다. (서민들 “평생 월세만 살라는 소리” 울분 … 주거사다리 걷어찬 ‘전세보증 70%’, “‘전세→월세’, 더 빨라지나”…’전세 에스크로’ 뭐길래).

- 그렇기 때문에 저희 자이랜드는 사후 규제가 아닌, 신뢰할 수 있는 평가 인프라를 먼저 구축해야 한다고 강조합니다. 그래야 시장 왜곡 없이 위험을 근본에서 줄이고, 서민에게 부담을 떠넘기지 않을 수 있습니다

- 왜곡된 평가 때문에 보증보험 가입도 점점 어려워져 세입자들이 무방비 상태에 놓입니다.

- 박민규 의원은 최근 “전세사기 예방 취지는 이해하지만, 급격한 제도 변화는 서민 주거 안정에 부정적 영향을 준다”고 지적하며 HF의 산정 방식을 실제 거래가에 더 가깝게 조정해야 한다고 촉구했습니다 (“전세대출 막혀” “보증금 못 돌려줘”…보증 문턱 높인 HF, 빌라시장 비명).

- 박민규 의원은 최근 “전세사기 예방 취지는 이해하지만, 급격한 제도 변화는 서민 주거 안정에 부정적 영향을 준다”고 지적하며 HF의 산정 방식을 실제 거래가에 더 가깝게 조정해야 한다고 촉구했습니다 (“전세대출 막혀” “보증금 못 돌려줘”…보증 문턱 높인 HF, 빌라시장 비명).

- 불과 지난주에도 HUG가 청년안심주택 보증보험 갱신을 거절했습니다. 기존 감정평가액이 20% 가까이 낮게 책정된 탓에 청년 세입자들이 보증금 반환 불안에 놓이고, 청년주택 공급 자체가 흔들리는 사례가 발생했습니다. 보호 장치가 오히려 배제 장치가 된 아이러니입니다 (전세사기 뺨 맞은 국토부·HUG…청년주택에 감정가 ‘20% 룰’ 씌웠다).

- 빌라·다가구 임대인과 세입자는 공시가격 기준을 충족하지 못해 보증보험 가입이 막히고, 계약 취소·보증금 미반환 피해로 이어지고 있습니다.

- 한국임대인연합도 “비(非)아파트 임대인은 서민 주거의 최전선인데, 제도가 오히려 희생양으로 만들고 있다”고 호소했습니다 (“전세보증 안돼” 세입자 외면…뿔난 빌라 집주인들, 여의도 몰려간다).

- 다른 보고서에 따르면 주택 소유주로부터 대체 평가 방법에 대한 수요가 있습니다. ([서미숙의 집수다] 비아파트 6년 임대 시행 한 달…빌라 공급 살아날까).

- 감정평가 방식은 비용도 크고 결과도 들쑥날쑥해 서민이 접근하기 어렵습니다. 일부 은행은 ‘업무 부담’을 이유로 아예 빌라 실수요자의 감정평가 신청을 거절하기도 합니다 (디딤돌대출 빌라 감평 거절하는 은행들… 실수요자들 “매매 안 되는 이유 알겠다” 한숨).

저희의 해법

저는 자이랜드의 독립형 자동가치산정모형(AVM)을 소개했습니다.

이 시스템은 모든 주택 유형에서 객관적이고 투명하며 저비용의 평가를 제공합니다.

- 다른 시세체계와 달리 저희는 지역·주택유형별 오차율을 공개하여, 모델의 강점과 개선 필요 지점을 누구나 확인할 수 있도록 합니다.

- 특히 부동산원테크시세가 아파트에 집중하는 반면, 저희 자이랜드 AVM은 빌라, 다세대, 지역주택까지 확장 적용합니다. 바로 그동안 금융 소외가 가장 심했던 자산군입니다.

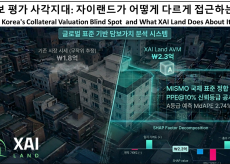

저희는 2025년 5월, 6,000건의 빌라 매매 실거래가를 대상으로 테스트했습니다. 그 결과:

- 부동산원테크시세 대비 20% 더 넓은 시장 커버리지

- 실제 거래가 ±10% 이내의 엄격한 위험 허용범위에서 30% 더 높은 정확도

- 전체 거래 중 약 11%(654건)에서 부동산원테크시세가 놓친 평가 보완

또한 위험 관리 강화를 위해, 저희는 Confidence Grading(신뢰도 등급)과 SHAP 값 설명을 AVM 결과에 통합하고 있습니다.

- 신뢰도 등급은 각 평가의 신뢰도를 점수로 표시해 금융기관이 결과를 그대로 활용할지, 추가 실사·감정평가를 할지 판단하도록 돕습니다.

- SHAP 값은 특정 부동산 평가에서 어떤 요인(입지, 건물유형, 최근 거래 패턴 등)이 영향을 미쳤는지 설명해 투명성과 감사 가능성을 보장합니다.

이를 통해 금융기관은 기존보다 낮은 시스템 리스크로 더 많은 대출, 보증, 연금을 취급할 수 있습니다. 청년·고령층·저소득 가구에게는 안전하고 접근 가능한 금융 기회가 현실로 열리게 됩니다.

필요한 제도 개혁

현행 법은 제1금융권 은행만, 그것도 50세대 이하 주택만 AVM 활용을 허용합니다.

저는 이 제한을 철폐해야 한다고 주장했습니다. 대규모 아파트 단지처럼 거래량이 많은 곳일수록 오히려 AVM의 정확성이 입증되기 때문입니다.

또한, 제2금융권·저축은행·지역 금융기관 등에도 AVM 활용을 확대해야 진정한 포용금융이 가능해집니다.

글로벌 사례

- 미국: 프레디맥은 이해상충 문제 때문에 외부 은행 제공용 AVM 서비스를 중단했습니다. 한국의 KB시세, 부동산원테크시세도 마찬가지로 이해상충 위험이 있습니다.

- 유럽 AVM 협회는 “가격지수는 흐름만 보여줄 뿐, 개별 자산 가치를 정확히 평가할 수 없다”고 명확히 밝혔습니다. 현재 HF가 주택연금 계리모형 재설계를 진행 중인 상황에서 매우 중요한 시사점을 줍니다.

왜 중요한가

토론 과정은 고무적이었습니다. 국회의원·규제기관 관계자들 사이에서 “한국의 법이 바뀌어야 한다”는 공감대가 형성되었습니다.

동시에 이런 우려도 제기되었습니다. “AVM 규제를 완화하면, 위험은 누가 감당하고 감정평가사 역할은 어떻게 되는가?”

저는 이 질문을 매우 중요하게 생각합니다. 그리고 글로벌 사례는 분명한 답을 줍니다.

- 미국: 6개 연방기관이 AVM에 대해 정확성·편향 방지·이해상충 회피·감사 가능성을 의무화한 품질관리기준(QCS)을 도입했습니다. AVM을 ‘위협’이 아니라 안전장치로 재정의한 것입니다.

- 호주: “AVM이 감정평가에 해당하느냐” 논쟁은 피하고, 금융기관이 자체적으로 robust한 Valuation Governance Framework를 증명하도록 요구했습니다.

- 캐나다: 감정평가사를 배제하지 않고, 데이터 검증과 복잡사례 담당 역할로 전환시켰습니다. AVM은 표준화된 저위험 거래를 처리했습니다.

앞으로의 방향

저는 이렇게 제안합니다:

- 50세대 제한 철폐 → 거래가 많아 정확도가 높은 곳에 AVM을 우선 적용

- K-QCS(한국형 품질관리기준) 도입 → 정확성, 데이터 무결성, 무작위 검증, 이해 상충 방지 포함

- 주의해야 할 충돌의 예:

- 은행이 소유한 AVM → 자체 AVM을 운영하는 은행은 대출을 확대하기 위해 부동산 가치를 과대평가하거나 위험 노출을 줄이기 위해 저평가하려는 유혹을 받을 수 있습니다.

- 은행 투자자가 있는 AVM → 은행 또는 금융 기관의 지원을 받는 제공업체는 투자자의 이익에 부합하기 위해 가치를 왜곡할 수 있습니다.

- 정부가 운영하는 AVM → 국가가 운영하는 AVM은 광범위한 정책 목표(예: 지역 개발을 촉진하기 위해 가치를 부풀리거나 투기를 억제하기 위해 가치를 축소)에 부합하는 방식으로 자산 가치를 평가하도록 압력을 받을 수 있습니다.

- 주의해야 할 충돌의 예:

- 역할 재정의 → 감정평가사는 하이브리드 평가(저신뢰 사례, 복잡사례, 데이터 검증)에 집중

- 미국, 캐나다, 호주에서는 AVM이 확장되어도 감정평가사가 일자리를 잃지 않았습니다. 그들의 역할은 부동산 데이터 검증, 상태 보고, 복잡한 평가, 품질 관리와 같은 하이브리드 및 고부가가치 기능으로 전환되었습니다.

- 약 5,000명의 공인 감정평가사와 1조 1,600억 원(약 8억 2,800만 달러) 규모의 감정평가 시장을 보유한 한국은 규모에 비해 세계에서 가장 큰 감정평가 산업 중 하나입니다. 감정평가사 1인당 평균 수익(≈US$165,000)은 이미 미국과 대등한 수준이며 캐나다나 호주보다 훨씬 높습니다.

| 나라 | 감정평가사 (명) | 시장 규모 (연 매출) | 1인당 매출 |

| 미국 | ≈66,715 | ≈US$11.3B | ≈US$170,000 (2억4천만원) |

| 한국 | ≈5,000 | ≈US$828M (1조 1629억원) | ≈US$165,000 (US$2억3천만원) |

| 호주 | ≈7,336 | ≈US$390.6 ($600.9M AUD) | ≈US$53,244 (7천5백만원) |

| 캐나다 | ≈5,500 | ≈US$570M (793.2M CAD) | ≈US$100,000 (1억4천만원) |

- 대부분의 감정평가사가 소규모 주거용 업무에 의존하는 미국과 달리, 한국 감정평가사의 업무량은 주택담보 및 거래 관련 감정평가와 같은 민간 부문에서 약 70%의 수요가 발생하고 나머지 약 30%는 공공 부문 업무(토지 보상, 정부 공시 등)가 차지하는 등 양상이 다르게 나뉘어져 있습니다. 그러나 한국의 민간 부문 업무는 일반적으로 고부가가치 공공 및 개발 프로젝트도 처리하는 대형 감정평가법인을 통해 이루어지기 때문에 미국에 비해 기업화되고 집중화된 시장이 형성되어 있습니다 (감정평가, 시장개선을 통해 새로운 활로 모색).

- 즉, 빌라, 다세대, 지역주택 등 일상적인 주거용 주택금융으로 AVM을 확대한다고 해서 국내 감정평가사의 생계가 붕괴되지는 않을 것입니다. 국내 감정평가 수요의 약 70%가 이미 모기지 담보 및 거래와 같은 민간 부문 감정평가에 묶여 있지만, 바로 이러한 영역이 AVM이 안전하게 표준화하고 비용을 절감할 수 있는 분야입니다.

- 반면 감정평가사는 재개발, 보상, 대기업 프로젝트와 같이 더 가치 있고 복잡한 업무에 재배치될 수 있으며 데이터 검증, 상태 보고, 모델 감사 등 새로운 하이브리드 역할을 창출할 수도 있습니다. 이러한 기능은 향후 K-QCS 표준에 따라 규제 당국이 전문성을 요구하게 될 분야입니다.

- 국제적으로 감정평가사는 점점 더 하이브리드 모델의 일부가 되고 있습니다. 미국에서는 표준화된 주택에 대한 감정평가 면제를 감정평가 전문가인 ‘부동산 데이터 수집가’와 결합하여 시행하고 있습니다. 캐나다에서는 감정평가사가 검증 역할에 통합되어 있습니다. 호주에서는 규제 당국이 은행에 책임을 떠넘기면서 거버넌스 프레임워크를 요구했지만 감정평가사는 복잡한 업무의 중심에 남겨두었습니다.

- 한국도 표준화된 담보 및 주택 사례에 대해 AVM을 사용하는 유사한 모델을 채택하면서 감정평가사를 감독, 복잡한 평가 및 전문 기능으로 격상시킬 수 있습니다.

- 위험 기준 연동 → 표준 대출은 AVM, 고가·복잡자산은 인간 감정평가 유지

이렇게 하면 한국은 안전하게 제도를 현대화하면서도 전문성을 존중할 수 있습니다.

맺으며

저는 “평가”가 단순한 숫자가 아니라 금융 기회의 출발점이라고 믿습니다.

AVM이 이 역할을 하려면, 반드시 투명하고, 독립적으로 운영되며, 공정해야 합니다. 그리고 규제기관은 누구도 배제되지 않고, 어떤 지역도 소외되지 않으며, 국민 누구도 뒤처지지 않도록 제도를 설계해야 합니다.

정책 입안자, 금융 기관 또는 업계 리더라면 이 운동에 동참해 주시기 바랍니다. 사람들이 신뢰할 수 있는 부동산 금융 시장을 만들기 위해 함께 노력합시다.

한국의 민간 시민으로서 집값 사기를 예방하고 공정한 부동산 가치 평가를 촉진하기 위한 활동에 동참하고 싶으신 분들은 금융소비자보호포럼을 주최한 (A) 민병덕 의원, (B) 유동수 의원 (C) 이강일 의원 중 한 분 또는 세 분께 연락해주시기 바랍니다.

또는 은행이나 대출/보증 파트너에게 감정평가를 요청할 때 다음 질문을 통해 가장 정확하고 공정하며 편견 없는 부동산 가치를 제공받을 수 있도록 하세요:

- 기관에서 부동산 가치를 평가할 때 어떤 AVM 또는 평가 방법을 사용하나요?

- 귀사의 AVM은 어떻게 정확성을 보장하며, 공개된 오류율은 얼마인가요?

- 가치 평가 모델이 다양한 가격대 또는 지역에서의 표본 크기 및 정확도와 같은 성과 지표를 공개하나요?

- 성능 및 정확도 메트릭은 어디에서 확인할 수 있나요?

- 실시간 시장 상황을 반영하기 위해 AVM은 얼마나 자주 업데이트되나요?

- AVM이 부동산 가치를 과대평가하거나 과소평가하는 경향이 있나요?

- 재무 리스크로 이어질 수 있는 평가 오류를 방지하기 위해 어떤 안전장치가 마련되어 있나요?

- 차입자 또는 투자자가 AVM 평가에 동의하지 않는 경우, 이를 검토하거나 이의를 제기할 수 있는 절차는 무엇인가요?

- 귀 기관은 정확도 및 지역별 오류율 등 모델 성과 지표를 공개적으로 공유하는 자이랜드와 같은 AVM 제공업체의 사용을 고려하십니까? 그렇지 않다면 현재 사용 중인 AVM의 공개적으로 사용 가능한 성능 데이터를 공유할 수 있나요?

이러한 대화에 참여함으로써 주택 시장을 형성하는 기관에서 투명성을 높이고 더 나은 재무 의사 결정을 내리는 데 도움을 줄 수 있습니다.

자이랜드(주)에 대하여

자이랜드는 한국인이 어디에 있든 사기, 불공정 관행, 과다 청구의 위험 없이 완전한 투명성을 바탕으로 안심하고 부동산 금융과 거래를 할 수 있는 세상을 꿈꿉니다.

가장 정확한 AVM을 통해 부동산 거래를 지원하며, 정확한 가치 평가와 투명한 거래 프로세스를 보장하는 것이 우리의 사명입니다. 우리는 부동산 사기를 예방하고 공정한 가격을 보호하며, 국내외 모든 부동산 관련 과정에서 원활하고 안전한 경험을 제공하기 위해 끊임없이 노력하고 있습니다.

더 자세한 내용을 원한다면, https://xai.land/ 를 방문하거나 LinkedIn ( https://www.linkedin.com/company/18522292/ ) 또는 Facebook ( https://www.facebook.com/xailand/ )의 업데이트를 팔로우하십시오.

주요 요약은 Linktree(https://linktr.ee/xai_land)에서도 한눈에 확인하실 수 있습니다.

Why Independent AVMs Are Essential for Inclusive Finance in Korea: XAI Land’s presentation at South Korea’s National Assembly

On September 26, 2025, I had the honor of speaking at the National Assembly forum, “Inclusive Finance 3.0 Era: Direction and Implementation Strategy for Inclusive Finance for the Financially Excluded.” The forum was hosted by the offices of Representatives Min Byung-duk, Yoo Dong-soo, and Lee Gang-il and organized by the Finance and Happiness Network, the Senior Financial Education Council, and the Korea Financial Welfare Policy Institute.

In addition, regulators from the Financial Services Commission (FSC) and Financial Supervisory Service (FSS), executives from banks and finance related associations, and leaders from citizens groups all gathered to discuss how South Korea can build a financial system that is both more inclusive and more resilient.

I was invited as one of the case presenters to speak about the future of housing valuation and real estate finance in South Korea under the topic “Inclusive Collateral Valuation 3.0: Enabling inclusive finance with independently operated AVMs”.

My core message was simple: without transparent, independent, and fair housing valuations, South Korea cannot achieve true financial inclusion and will still be susceptible to appraisal related financial accidents and Jeonse fraud (I had the privilege of presenting on how AVMs could prevent Jeonse fraud in February 2025).

I am publishing my full National Assembly presentation so anyone can see exactly what we argued with related research.

What I Said

- Current system failures: Korea’s valuation system is dominated by apartment-focused indices and subjective appraisals. This leaves out villas, single-family homes, and regional housing – exactly the homes most used by young people, seniors, and low-income families.

- Seniors in detached or villa housing are blocked from enrolling in reverse mortgages or see their monthly payouts reduced because the system relies on outdated official tax-related prices (공시가격).

- Hwang In-do, Bank of Korea Research Head (황인도 한국은행 연구실장) also warned this is a major barrier to expanding the private reverse mortgage market (12억 넘어도 가능한 ‘주택연금’이라더니 “아파트만” 가입… “단계적 확대 검토”).

- Hwang In-do, Bank of Korea Research Head (황인도 한국은행 연구실장) also warned this is a major barrier to expanding the private reverse mortgage market (12억 넘어도 가능한 ‘주택연금’이라더니 “아파트만” 가입… “단계적 확대 검토”).

- Young people and first-time renters face inflated KB시세 and appraisal values, which contribute to Tin-can Jeonse (깡통전세) and Jeonse fraud. Higher artificial valuations also push up monthly rents, forcing low-income households into unsustainable burdens (“KB시세는 호가에 불과”…HUG 전세보증 사고 터지는 진짜 이유, 부동산원도 KB도 다 틀렸다…한계 드러낸 집값 ‘주간조사’, 자이랜드 AVM, K*시세·질로우 제쳤다… 정확도 2배 이상 높아, KB 부동산 시세, 실제보다 높다?, 서민들 “평생 월세만 살라는 소리” 울분 … 주거사다리 걷어찬 ‘전세보증 70%’).

- Although I did not get to mention this at the National Assembly, I recognize that institutions like HUG(주택도시보증공사) and HF(한국주택금융공사) are trying to curb Tin-can jeonse fraud (깡통전세) through stricter guarantees and lower LTVs. But as recent reports show, these measures risk pushing families into Half-jeonse (반전세) or monthly rental (월세) contracts, effectively cutting off the housing ladder they rely on. Likewise, escrow (에스크로) has been proposed as another protective measure, but experts warn it may only accelerate the shift toward monthly rental contracts (월세화) (서민들 “평생 월세만 살라는 소리” 울분 … 주거사다리 걷어찬 ‘전세보증 70%’, “‘전세→월세’, 더 빨라지나”…’전세 에스크로’ 뭐길래).

- That’s why at XAI Land believe the true solution is not just stricter rules after the fact, but building a reliable valuation infrastructure so risks are reduced at the source without distorting the market or shifting the burden onto ordinary citizens.

- Guarantee insurance becomes harder to access under these distorted valuations, leaving tenants unprotected.

- Rep. Park Min-gyu (박민규 의원) recently acknowledged that “while preventing Jeonse fraud is important, overly abrupt system changes undermine housing stability for ordinary people,” and called for HF’s pricing method to be brought closer to actual transaction prices (“전세대출 막혀” “보증금 못 돌려줘”…보증 문턱 높인 HF, 빌라시장 비명).

- Rep. Park Min-gyu (박민규 의원) recently acknowledged that “while preventing Jeonse fraud is important, overly abrupt system changes undermine housing stability for ordinary people,” and called for HF’s pricing method to be brought closer to actual transaction prices (“전세대출 막혀” “보증금 못 돌려줘”…보증 문턱 높인 HF, 빌라시장 비명).

- HUG denied renewal of youth housing guarantee insurance because traditional appraisals undervalued properties by nearly 20%. That decision destabilized existing tenants and jeopardized youth housing supply – an example of a system meant to protect citizens that ironically excluded them (전세사기 뺨 맞은 국토부·HUG…청년주택에 감정가 ‘20% 룰’ 씌웠다).

- Landlords and tenants in villas and multi-family homes are unable to meet public appraisal-based criteria for guarantee insurance, leading to cancelled contracts and unrecovered deposits.

- Even the Korean Landlord Federation (한국임대인연합) stated: “Non-apartment landlords, who are on the front line of affordable housing, are becoming scapegoats of the system.” (“전세보증 안돼” 세입자 외면…뿔난 빌라 집주인들, 여의도 몰려간다).

- According to other reports there is demand from homeowners about alternative valuation methods to be utilized ([서미숙의 집수다] 비아파트 6년 임대 시행 한 달…빌라 공급 살아날까).

- Appraiser-led valuations are not only costly but inconsistent, making them inaccessible for working families. Some banks even refuse villa buyers’ appraisal requests outright, citing “workload burden (디딤돌대출 빌라 감평 거절하는 은행들… 실수요자들 “매매 안 되는 이유 알겠다” 한숨).

- Seniors in detached or villa housing are blocked from enrolling in reverse mortgages or see their monthly payouts reduced because the system relies on outdated official tax-related prices (공시가격).

- Our solution: I introduced XAI Land’s independent Automated Valuation Model (AVM), which provides objective, transparent, and cost-efficient valuations across all housing types. Unlike others, we publish error rates by region and property class so people can see where our model is strong and where it needs improvement. Importantly, while systems like Real Estate Tech (부동산원테크시세) focus almost exclusively on apartments, XAI Land’s AVM extends coverage to villas, multi-family homes, and regional housing – precisely the asset classes where financial exclusion has been most severe.

- In fact, we tested our model on 6,000 villa transactions (연립·다세대 매매 실거래가, May 2025) and found:

- 20% broader market coverage than 부동산원테크시세

- 30% higher accuracy within a strict ±10% tolerance range around actual transacted values

- 11% of all tested transactions where our AVM delivered valuations that 부동산원 evaluated properties inaccurately.

- To further strengthen risk management, we are integrating confidence grading and SHAP value explanations into our AVM outputs.

- Confidence grading assigns a reliability score to each valuation, signaling to banks and insurers when an AVM result is statistically robust – or when the case should trigger enhanced due diligence.

- SHAP values explain which features (location, building type, recent transaction patterns, etc.) most influenced a specific property’s valuation, making the process transparent and auditable.

- Confidence grading assigns a reliability score to each valuation, signaling to banks and insurers when an AVM result is statistically robust – or when the case should trigger enhanced due diligence.

- This means financial institutions can underwrite more loans, more guarantees, and more reverse mortgages with lower systemic risk compared to existing methods. For youth, seniors, and low-income households, that translates into real access to safe and affordable housing finance.

- In fact, we tested our model on 6,000 villa transactions (연립·다세대 매매 실거래가, May 2025) and found:

- Legal policy reform needed: Current rules allow only Tier 1 banks to use AVMs and only for properties under 50 households. I argued that these restrictions should be lifted, since AVMs can be accurate in large apartment complexes with many transactions. Expanding AVM use to savings banks, regional/alternative lenders is essential for financial inclusion.

- Global precedent: I shared the case of Freddie Mac in the U.S., which had to stop offering its AVM to external banks due to conflict-of-interest risks. South Korea faces a similar issue with KB시세 and 부동산원테크시세, which may have conflicts of interest in providing valuations.

I also pointed to the position of the European AVM Association, which has made it clear: price indices only show trends, they cannot accurately assess the value of an individual asset. This distinction is critical. In Korea, institutions like HF are in the middle of redesigning their housing pension actuarial models. If they continue relying only on indices or appraisals that don’t capture true property-level values, they risk undermining both financial stability and consumer trust.

Why It Matters

The discussion that followed was encouraging. An unspoken consensus among attendees including lawmakers and regulators agreed that Korea’s laws may need to change.

At the same time, a concern was raised: “If we deregulate AVM usage, what about the risks and the appraisal profession’s role?” This is an important question and one we at XAI Land take seriously.

Here is how global best practice addresses it:

- United States – Mandatory Quality Control Standards (QCS): Six federal agencies required AVMs to meet strict standards on accuracy, anti-bias, conflict avoidance, and auditability. This reframed AVMs not as a “threat” but as a regulatory safeguard against appraisal bias and inflated valuations.

- Australia – Governance-first approach: Regulators sidestepped debates about whether AVMs “count” as valuations, by focusing on institutional accountability. Financial institutions must prove that their valuation governance is robust, regardless of tool.

- Canada – Co-option strategy: Instead of excluding appraisers, regulators created hybrid roles. Appraisers shifted into property-data verification and complex cases, while AVMs handled standardized, lower-risk transactions.

From these lessons, I believe Korea should:

- Remove the 50-household limit and prioritize AVM use where accuracy is empirically strongest (large apartment complexes).

- Adopt Korean Quality Control Standards (K-QCS): focusing on accuracy, data integrity, random testing, and preventing conflicts of interests.

- Examples of conflicts to guard against:

- Bank-owned AVMs → A bank running its own AVM may be tempted to overvalue properties to expand lending, or undervalue them to reduce risk exposure.

- AVMs with bank investors → Providers backed by banks or financial institutions may skew valuations to align with investor interests.

- Government-operated AVMs → State-run AVMs can be pressured to value assets in ways that serve broader policy goals (e.g., inflating values to boost regional development, or deflating values to curb speculation).

- Examples of conflicts to guard against:

- Redefine roles: Allow appraisers to transition into hybrid valuation roles, focusing on verifying condition data and handling complex cases where AVMs may provide valuations that could be deemed as “Low Confidence”.

- In the U.S., Canada, and Australia, appraisers did not “lose jobs” when AVMs scaled. Their roles shifted into hybrid and higher-value functions such as property data verification, condition reporting, complex valuations, and quality control.

- South Korea, with ~5,000 licensed appraisers and an appraisal market worth ≈₩1.16조 (≈US$828M), is among the largest appraisal industries in the world relative to its size. The average revenue per appraiser (≈US$165,000) is already on par with the U.S. and well above Canada or Australia.

| Country | Estimated Appraisers | Market Size (Annual Revenue) | Average Revenue per Appraiser |

| USA | ≈66,715 | ≈US$11.3B | ≈US$170,000 (2억4천만원) |

| South Korea | ≈5,000 | ≈US$828M (1조 1629억원) | ≈US$165,000 (US$2억3천만원) |

| Australia | ≈7,336 | ≈US$390.6 ($600.9M AUD) | ≈US$53,244 (7천5백만원) |

| Canada | ≈5,500 | ≈US$570M (793.2M CAD) | ≈US$100,000 (1억4천만원) |

- Unlike the U.S., where most appraisers depend on small-scale residential assignments, Korean appraisers’ workload is split differently: around 70% of demand comes from private-sector valuations such as mortgage collateral and transaction-related appraisals, while public-sector work (land compensation, government disclosures, etc.) makes up the remaining ~30%. However, these private-sector assignments in Korea are typically channeled through large appraisal corporations that also handle high-value public and development projects, creating a more concentrated, corporatized market compared to the U.S.

- This means that expanding AVMs into routine residential housing finance (e.g., villas, multi-family, regional housing) would not collapse Korean appraisers’ livelihood. While around 70% of Korea’s appraisal demand is already tied to private-sector valuations such as mortgage collateral and transactions, these are precisely the areas where AVMs can safely standardize and reduce costs (감정평가, 시장개선을 통해 새로운 활로 모색).

- By contrast, appraisers can be redeployed to higher-value and complex assignments such as redevelopment, compensation, and large corporate projects while also creating new hybrid roles in data verification, condition reporting, and model auditing. These functions are exactly where regulators will demand expertise under future K-QCS standards.

- Internationally, appraisers are increasingly part of hybrid models. In the U.S., appraisal waivers for standardized homes are paired with “property data collectors,” often drawn from the appraisal profession. In Canada, appraisers are integrated into verification roles. In Australia, regulators pushed the responsibility to banks, requiring governance frameworks but leaving appraisers central in complex assignments.

- Korea can adopt a similar model using AVMs for standardized collateral and housing cases while elevating appraisers into oversight, complex valuations, and specialized functions.

- Tie AVM results to risk thresholds: For routine loans, use AVMs; for luxury, complex properties, or properties where AVMs are yielding “Low Confidence” intervals in, keep human appraisals.

By doing this, Korea can modernize safely while respecting professional expertise.

What’s Next

At XAI Land, I believe valuation is not just a number. It is the foundation of financial opportunity. For AVMs to serve this role, they must be transparent, independently run/operated, and fair – and regulators must design the system so that no citizen is excluded, no region is ignored, and no one is left behind.

If you are a policymaker, financial institution, or industry leader, I urge you to join this movement. Let’s work together to build a real estate finance market that people can trust.

If you are private citizen living in South Korea who may wish to be support our initiatives above to expand financing to those who may be in need then please contact one if not all of the representatives who hosted this forum – (A) Min Byung-duk, (B) Yoo Dong-soo, (C) Lee Gang-il:

Alternatively, ask your bank or lending partner any of the following questions when you may ask them for an appraisal to ensure you’re being offered the most accurate, fair, and unbiased real estate valuation:

- What AVM or valuation method does your institution use to assess property values?

- How does your AVM ensure accuracy, and what is its published error rate?

- Does your valuation model disclose performance metrics, such as sample sizes and accuracy at different price points or regions?

- Where can I see their performance and accuracy metrics?

- How often is the AVM updated to reflect real-time market conditions?

- Does the AVM tend to overestimate or underestimate property values?

- What safeguards are in place to prevent valuation errors that could lead to financial risks?

- If a borrower or investor disagrees with an AVM valuation, what is the process for reviewing or challenging it?

- Would your institution consider using an AVM provider like XAI Land, which publicly shares model performance metrics, including accuracy rates and regional error rates? If not, can you share publicly available performance data from the AVM currently in use?

Thank you for your support, and I look forward to continuing this important conversation.

About XAI Land

XAI Land envisions a world where Koreans, no matter where they may call home, can confidently finance and transact real estate with complete transparency, free from the risks of fraud, unfair practices, or being ripped off.

Our mission is to support real estate transactions with the most accurate automated valuation models (AVMs), ensuring accurate valuations and transparent transaction processes. We are constantly striving to prevent real estate fraud, protect fair prices, and provide a seamless and secure experience in all real estate-related processes, both domestically and internationally.

For more information, visit https://xai.land/ or follow updates on LinkedIn (https://www.linkedin.com/company/18522292/) or Facebook (https://www.facebook.com/xailand/).

You can also see the main summary at a glance on Linktree (https://linktr.ee/xai_land).

You Might Like